Why Every FinTech Startup in India Is Betting Big on UPI 3.0 — And What You’re Missing

Picture this scenario: A small business owner in Bengaluru applies for a loan at 10 AM, gets instant approval by 10:05 AM, and starts spending the credit line through UPI by 10:10 AM. No paperwork, no branch visits, no waiting for weeks. This is not a futuristic dream—this is happening right now, and it is reshaping how India thinks about credit, lending, and financial services.

India is now home to 28 fintech unicorns, ranking third globally behind the US and China, and almost every single one of them is doubling down on UPI 3.0 capabilities. But what exactly is driving this massive shift, and why are startups betting their entire business models on this evolution?

The UPI Revolution That Started It All

UPI transformed payments in India by making digital transactions as simple as sending a text message. From processing a handful of transactions in 2016 to handling billions of transactions monthly, UPI became the backbone of India’s digital economy. But payments were just the beginning.

NPCI started introducing new features under UPI 3.0 from 2024, including “Conversational Voice Payments” unveiled at the Global Fintech Fest 2024, marking a significant advancement in transaction convenience. However, the real game-changer lies not in how we pay, but in how UPI 3.0 is revolutionizing lending, credit scoring, and customer onboarding.

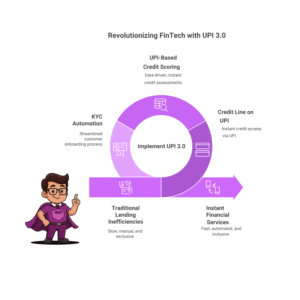

The Credit Line Revolution: Instant Money at Your Fingertips

The most significant development in UPI 3.0 is the Credit Line on UPI feature. This product empowers individuals and small businesses to obtain pre-sanctioned credit lines from banks, which can be utilized immediately for transactions through UPI. Think of it as having a pre-approved credit card that works seamlessly with UPI payments.

Here is how the process works in practice: Users open a UPI app, go to the Credit or Loan section, select the ‘Credit Line option’, enter required personal and financial information, and complete KYC verification. What previously took weeks now happens in minutes.

This capability is transforming how FinTech startups approach lending. Instead of building separate loan applications and payment systems, they can now offer instant credit that integrates directly with India’s most popular payment method. The result is a seamless user experience that removes friction from both borrowing and spending.

Micro-Lending Gets a Major Upgrade

UPI 3.0 is particularly revolutionary for micro-lending startups. Traditional micro-lending involved extensive paperwork, physical verification, and lengthy approval processes. The new UPI infrastructure changes this completely.

India has launched a digital credit assessment system for MSMEs with UPI-based lending, replacing traditional collateral with transaction-based assessments. This means that small businesses can now access credit based on their UPI transaction history rather than traditional collateral or credit scores.

For FinTech startups, this opens up massive opportunities. They can now offer:

Instant micro-loans based on UPI transaction patterns Credit lines that activate automatically when users need them Small business loans that get approved based on payment volumes Consumer credit that adapts to spending behavior

The addressable market is enormous. Small businesses and individual entrepreneurs who were previously excluded from formal credit systems can now access funding instantly through platforms they already use daily.

Instant Credit Scoring: The Data Goldmine

Perhaps the most exciting aspect of UPI 3.0 for FinTech startups is the treasure trove of transaction data it provides for credit scoring. Traditional credit scoring in India relied heavily on formal banking relationships and credit card usage, excluding millions of people with limited banking history.

UPI transaction data tells a completely different story. It reveals:

Regular income patterns through salary credits and recurring payments Spending behavior across different categories Business cash flows for merchants and service providers Financial discipline through savings and investment patterns Social connections through peer-to-peer transactions

FinTech startups are building sophisticated algorithms that can assess creditworthiness within minutes using this UPI transaction data. A street vendor who receives consistent UPI payments can now qualify for business loans. A young professional with regular UPI-based salary credits can access instant personal loans without a lengthy credit history.

The competitive advantage is clear: startups that master UPI-based credit scoring can approve loans faster, assess risk more accurately, and serve previously underbanked populations.

KYC Automation: The Silent Game Changer

Customer onboarding has always been a pain point for FinTech startups. Traditional KYC processes involved document submissions, manual verification, and regulatory compliance checks that could take days or weeks. UPI 3.0 changes this equation dramatically.

As per April 2021 RBI directive, after March 31, 2022, all KYC compliant digital wallets became interoperable using the UPI system. This interoperability means that KYC verification done for one UPI-enabled service can be leveraged across multiple platforms.

For FinTech startups, this translates to:

Instant customer verification using existing UPI KYC data Reduced onboarding friction and higher conversion rates Lower compliance costs and faster regulatory approvals Seamless integration with banking partners who are already UPI-enabled

The automation possibilities are endless. A customer who is already KYC-verified on one UPI app can instantly access services from multiple FinTech partners without repeating the verification process.

The Platform Play: Why Infrastructure Matters

M2P Fintech serves as a solution for enabling credit line functionality on UPI with their unified credit stack, empowering financial institutions with flexible lending solutions across various channels. This highlights how FinTech startups are not just building consumer-facing applications but also creating the infrastructure that enables UPI 3.0 capabilities.

The smartest FinTech startups are positioning themselves as enablers rather than just service providers. They are building:

API platforms that help traditional banks offer UPI-based credit White-label solutions for smaller financial institutions Credit scoring engines that can be licensed to multiple lenders KYC automation tools that serve the entire ecosystem

This platform approach creates multiple revenue streams and reduces dependency on any single business model.

Market Dynamics: The Numbers Tell the Story

The India Fintech Market is expected to reach USD 44.12 billion in 2025 and grow at a CAGR of 16.65% to reach USD 95.30 billion by 2030. This growth is being driven primarily by UPI-enabled innovations.

FinTech companies in India raised $899M in equity funding across 111 rounds till June 2025, with a significant portion of this funding going to startups building on UPI 3.0 capabilities.

The funding pattern reveals investor confidence in UPI-based business models. Startups that can demonstrate strong UPI integration and innovative use cases are attracting premium valuations.

What You Are Missing: The Strategic Implications

If you are not paying attention to UPI 3.0, you are missing several critical opportunities:

Speed as a Competitive Advantage: In a market where loan approval time can be the difference between winning and losing customers, UPI 3.0 enables instant decisions that traditional systems cannot match.

Data-Driven Insights: UPI transaction data provides insights into customer behavior that were previously impossible to obtain. This data advantage translates directly into better risk assessment and product development.

Network Effects: As more services integrate with UPI 3.0, the platform becomes more valuable for everyone. Early movers benefit from stronger network effects and better positioning.

Regulatory Alignment: Building on UPI 3.0 means working within a framework that has strong regulatory support and government backing, reducing compliance risks.

Scale Opportunities: UPI 3.0 infrastructure can handle massive transaction volumes, enabling startups to scale rapidly without rebuilding core systems.

The Future Landscape: What Comes Next

The evolution is far from over. We are seeing early signs of even more advanced capabilities:

Voice-based lending applications using UPI 3.0 conversational features AI-driven credit decisions happening in real-time during transactions Cross-border lending capabilities for Indian businesses expanding globally Integration with emerging technologies like blockchain for transparent credit scoring

Industry stakeholders predict a more positive period in 2025 for the Indian FinTech ecosystem, largely driven by innovations built on UPI 3.0.

The Bottom Line: Why This Matters Now

UPI 3.0 is not just another technology upgrade—it represents a fundamental shift in how financial services work in India. FinTech startups that understand and leverage these capabilities will define the next decade of financial innovation.

The window of opportunity is open now, but it will not stay open forever. As more startups build sophisticated UPI 3.0-based solutions, the competitive landscape will become increasingly challenging for late entrants.

The question is not whether UPI 3.0 will transform financial services—it is already happening. The question is whether your business will be part of this transformation or left behind by it.

For FinTech entrepreneurs, investors, and anyone building in the financial services space, understanding UPI 3.0 is not optional—it is essential. The startups that master these capabilities today will become the financial infrastructure of tomorrow.

The revolution is here. The only question left is: are you ready to be part of it?