Picture this: A small business owner in Pune applies for a loan at 2 PM on a Tuesday. By 4 PM that same day, they receive approval, complete with personalized terms tailored to their specific risk profile. No endless paperwork. No weeks of waiting. No human bias in the decision-making process.

This isn’t a glimpse into some distant future—it’s happening right now across India’s financial landscape. AI has moved from boardroom buzzword to operational reality, fundamentally transforming how lenders assess risk, approve loans, and protect themselves from fraud.

The numbers tell a compelling story: 62% of executives recognize artificial intelligence/machine learning technology (AI/ML) is elevating underwriting quality and reducing fraud, and the results are already visible in the bottom line.

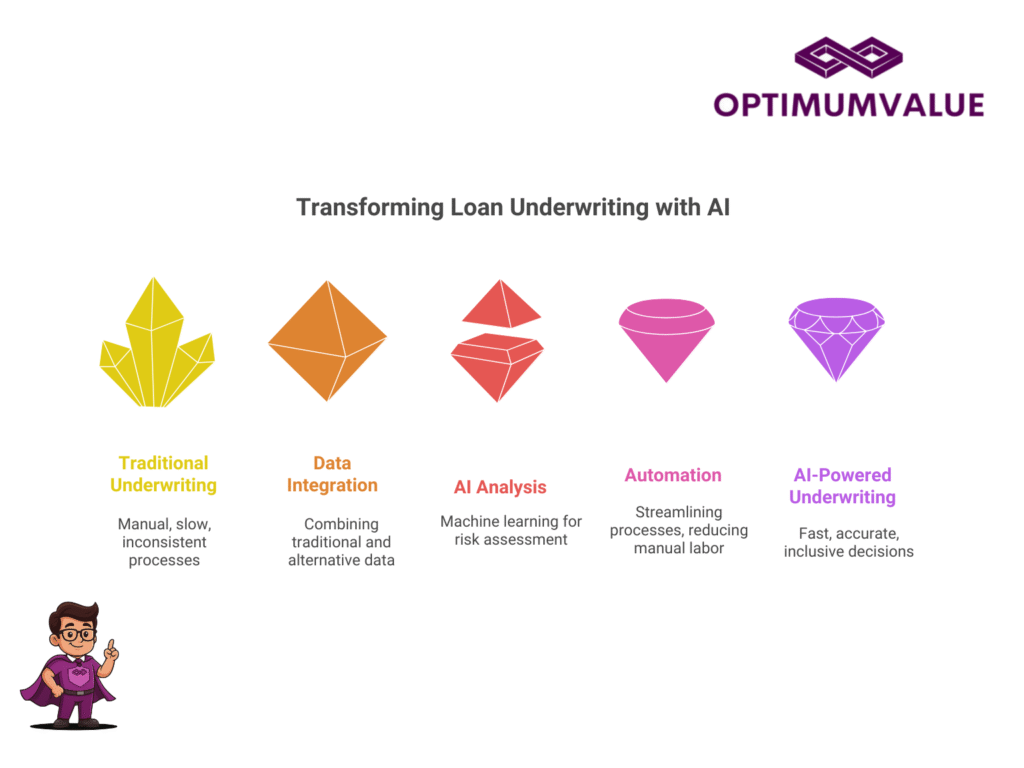

The Traditional Underwriting Problem: Slow, Expensive, and Often Wrong

For decades, loan underwriting has been a bottleneck in the lending industry. Traditional methods rely heavily on manual processes, limited data points, and human judgment—a combination that creates several pain points:

Manual credit assessment can take days or weeks, leading to frustrated customers and lost business opportunities. Human underwriters, despite their expertise, can only process a fraction of the applications that AI systems handle daily. More concerning is the consistency issue—two underwriters might reach different conclusions about the same applicant.

Traditional systems also struggle with thin-file applicants—people with limited credit history who might be creditworthy but don’t fit conventional scoring models. In India, where a significant portion of the population lacks extensive credit records, this limitation has historically excluded millions from accessing formal credit.

How AI Is Revolutionizing Loan Underwriting Today

Lightning-Fast Decision Making

AI systems can analyze hundreds of data points in seconds, dramatically reducing approval times. What once took days now happens in minutes. This speed isn’t just about convenience—it’s about competitive advantage. Lenders who can provide instant decisions capture more customers and improve their market position.

Enhanced Risk Assessment Through Alternative Data

Modern AI systems don’t just look at traditional credit scores. They analyze smartphone usage patterns, utility payment histories, social media behavior, and transaction patterns to create a comprehensive risk profile. This approach has proven particularly effective in emerging markets like India, where traditional credit data might be limited.

Significant Cost Reduction

Automation eliminates much of the manual labor involved in underwriting. AI can shorten claims processing time by 30%, ensuring that policyholders receive their settlements quickly and reducing the administrative burden on insurers. While this statistic relates to insurance, similar efficiency gains are seen in loan processing.

Real Statistics: The Impact Is Measurable

The transformation isn’t just theoretical—the numbers prove AI’s effectiveness:

Fraud Detection Improvements: AI systems excel at identifying suspicious patterns that humans might miss. By analyzing vast datasets and recognizing subtle correlations, these systems can flag potentially fraudulent applications with remarkable accuracy.

Approval Rate Optimization: improved risk assessment models leading to a reduction in losses by up to 15%. This improvement comes from AI’s ability to identify creditworthy applicants who might be rejected by traditional systems, while simultaneously catching higher-risk applications that might otherwise slip through.

Processing Efficiency: The shift from manual to automated processes has reduced operational costs significantly while improving consistency in decision-making.

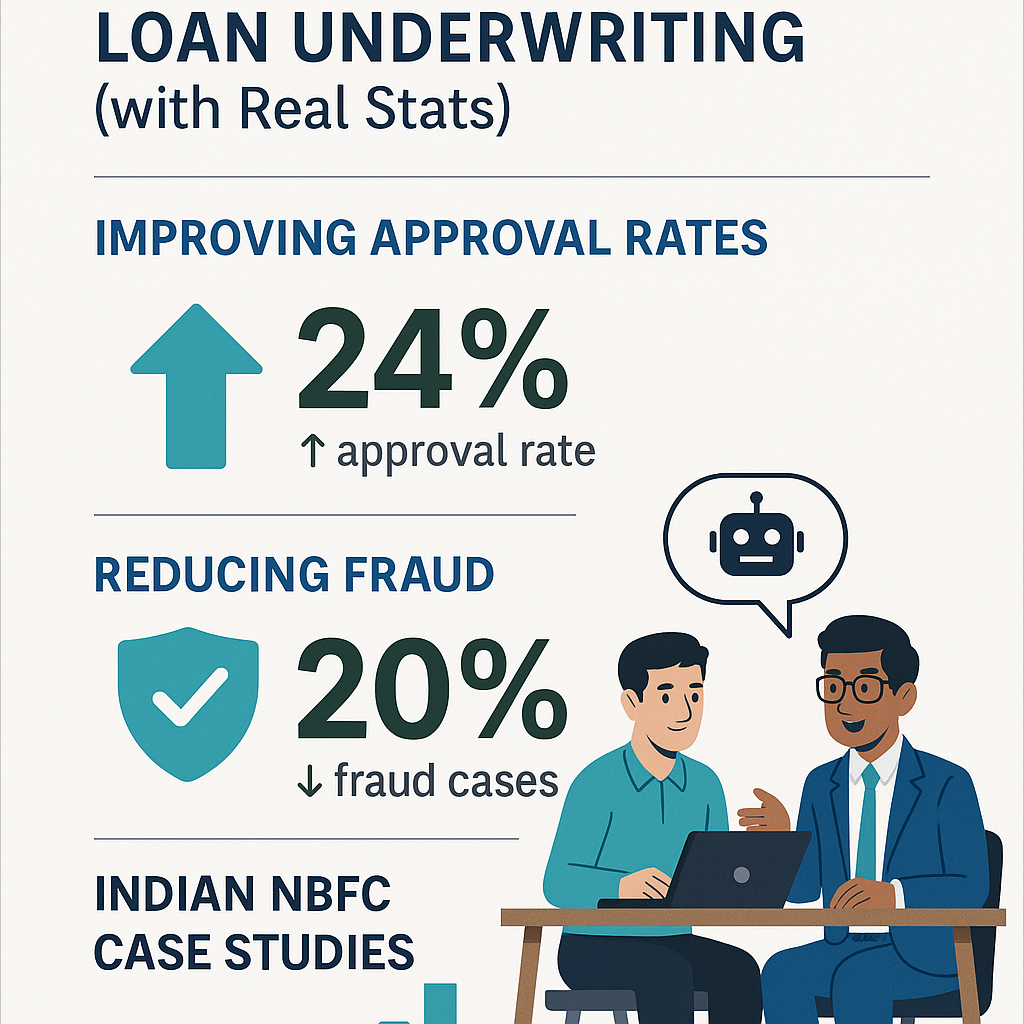

Indian NBFC Success Stories: AI in Action

Case Study 1: Digital Transformation at Scale

Findings indicate that AI has reached that tipping point in India, particularly in the NBFC-P2P lending space. Several Indian NBFCs have successfully implemented AI-driven underwriting systems, resulting in faster loan disbursals and improved risk management.

Case Study 2: Addressing Over-Indebtedness Concerns

The Indian lending landscape faces unique challenges. As of September 2024, 8% of borrowers had active loans from four or more lenders, a sharp rise from 3.6% in 2021. AI systems help NBFCs identify these over-leveraged borrowers by cross-referencing multiple data sources and providing a more complete picture of an applicant’s financial obligations.

Case Study 3: Serving the Underserved

Many Indian NBFCs focus on financial inclusion, extending credit to previously underserved segments. AI enables these institutions to assess risk more accurately for applicants with limited formal credit history by leveraging alternative data sources like mobile phone usage, utility payments, and digital transaction patterns.

The Technology Behind the Transformation

Machine Learning Models

At the heart of AI underwriting are sophisticated machine learning algorithms that continuously learn and improve. These models analyze historical loan performance data to identify patterns that predict repayment likelihood.

Natural Language Processing

AI systems can analyze unstructured data like customer communications, social media posts, and even voice patterns during phone conversations to assess creditworthiness and detect potential fraud.

Real-Time Data Integration

Modern AI platforms integrate data from multiple sources in real-time, including bank statements, GST returns, utility bills, and even psychometric assessments, creating a comprehensive applicant profile.

Overcoming Implementation Challenges

While the benefits are clear, implementing AI in underwriting isn’t without challenges:

Data Quality and Availability: AI systems are only as good as the data they process. Ensuring clean, relevant, and up-to-date data feeds is crucial for accurate decision-making.

Regulatory Compliance: Financial institutions must navigate complex regulatory requirements while implementing AI systems. Ensuring transparency and explainability in AI decisions is becoming increasingly important.

Change Management: Transitioning from traditional underwriting to AI-driven processes requires significant organizational change, including staff training and process redesign.

Looking Ahead: The Future Is Now

The transformation of loan underwriting through AI isn’t a future possibility—it’s today’s reality. Financial institutions that haven’t started their AI journey risk being left behind as competitors offer faster, more accurate, and more inclusive lending solutions.

The key to success lies in choosing the right technology partners and platforms that can seamlessly integrate with existing systems while providing the flexibility to evolve with changing market needs.

How Salesforce Can Accelerate Your AI Underwriting Journey

For organizations looking to implement or enhance their AI underwriting capabilities, Salesforce Financial Services Cloud offers a comprehensive platform that addresses the entire lending lifecycle.

Integrated Customer Data Platform: Salesforce’s Customer 360 provides a unified view of customer data from multiple sources, essential for AI-driven risk assessment. This integrated approach ensures that underwriting decisions are based on complete, accurate customer profiles.

AI-Powered Insights with Einstein: Salesforce Einstein AI can be configured to analyze lending patterns, predict default risks, and identify fraudulent applications. The platform’s machine learning capabilities continuously improve decision accuracy based on historical performance data.

Workflow Automation: Complex underwriting processes can be automated using Salesforce Flow, reducing manual intervention and accelerating approval times. This automation extends from initial application processing to final approval and disbursement.

Compliance and Audit Trail: Built-in compliance features ensure that all AI-driven decisions are properly documented and auditable, addressing regulatory requirements while maintaining operational efficiency.

Scalable Architecture: As lending volumes grow, Salesforce’s cloud-native architecture scales seamlessly, ensuring consistent performance even during peak application periods.

Integration Capabilities: Salesforce’s robust API ecosystem allows seamless integration with existing core banking systems, credit bureaus, and alternative data providers, creating a comprehensive underwriting ecosystem.

By leveraging Salesforce’s platform capabilities, financial institutions can accelerate their AI transformation while maintaining the flexibility to adapt to evolving market conditions and regulatory requirements.