The Buy Now, Pay Later (BNPL) revolution seemed like it happened overnight. One day we were fumbling for credit cards, the next we were splitting purchases into bite-sized installments with a few taps on our phones.

But here’s the thing about revolutions – they don’t stop evolving.

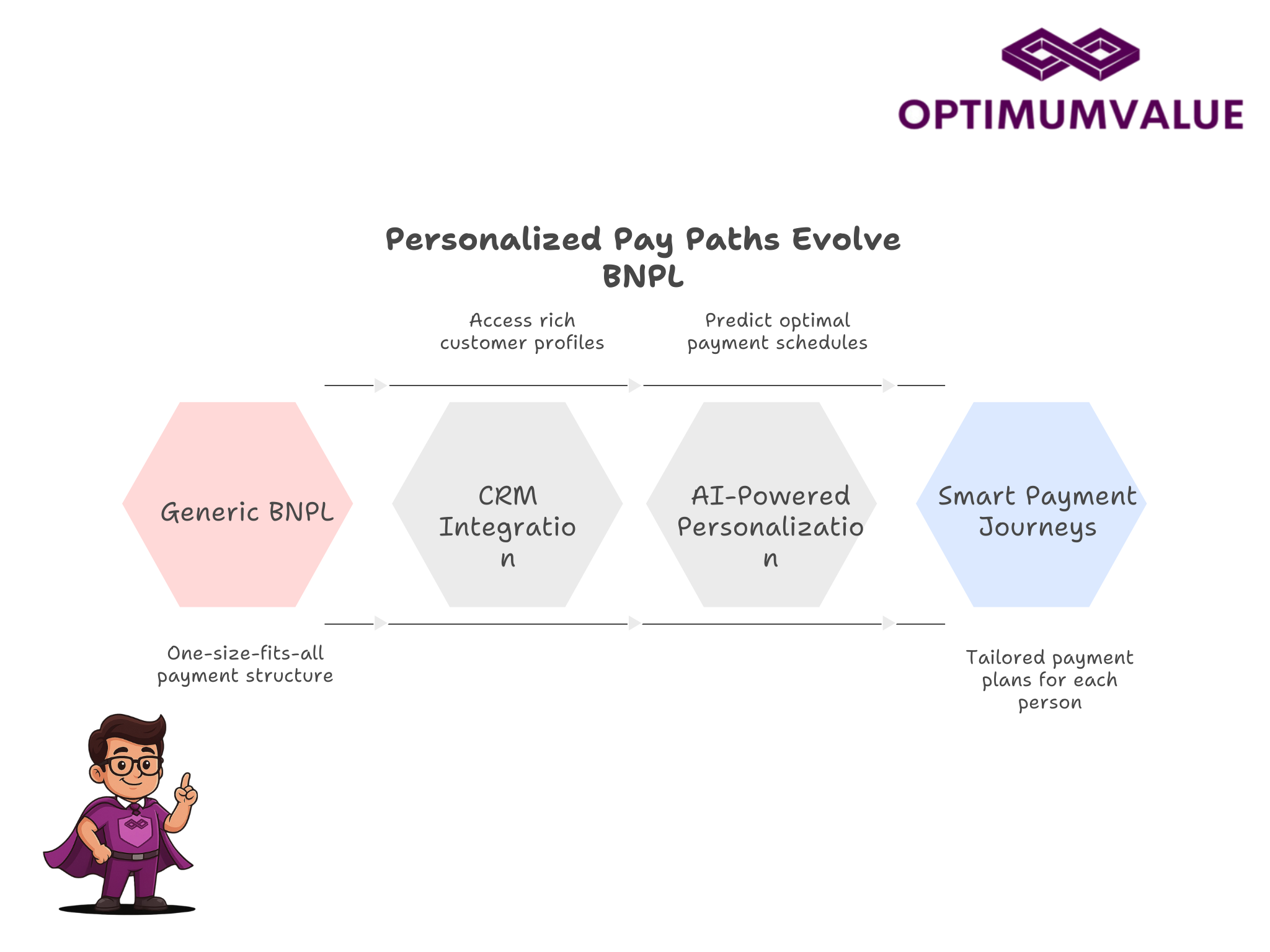

The BNPL landscape is shifting again, and this time it’s getting personal. Really personal. We’re moving from the one-size-fits-all “pay in 4” model to something far more sophisticated: Personalized Pay Paths.

The Problem with Generic BNPL

Traditional BNPL solutions treat all customers the same. Whether you’re buying a $50 pair of shoes or a $2,000 laptop, you get the same payment structure. It’s like giving everyone the same prescription glasses – sure, some people might see better, but most are still squinting.

This generic approach creates friction for both businesses and customers:

- High-value purchases often need longer payment terms

- Repeat customers deserve better flexibility than first-time buyers

- Different income cycles (weekly, bi-weekly, monthly) require different payment schedules

- Shopping behavior patterns vary dramatically across customer segments

Enter the New Wave: CRM + AI = Smart Payment Journeys

The next generation of BNPL platforms is cracking this code by combining two powerful technologies: Customer Relationship Management (CRM) data and Artificial Intelligence.

Here’s how it works:

Instead of offering everyone the same “4 payments over 6 weeks” option, these smart platforms analyze individual customer data to create tailored payment journeys. They look at purchase history, payment behavior, income patterns, and even seasonal spending habits to craft payment plans that actually make sense for each person.

Real-World Example

Imagine Sarah, a freelance designer who gets paid monthly, and Mike, a retail worker who gets paid weekly. Traditional BNPL would offer them identical payment schedules. But with personalized pay paths:

- Sarah gets monthly installments aligned with her freelance payment cycle

- Mike gets weekly micro-payments that match his paycheck schedule

- Both get payment amounts optimized for their spending capacity and history

The Technology Behind the Magic

CRM Integration: The Data Foundation

Modern BNPL platforms are integrating deeply with business CRM systems to access rich customer profiles. This includes:

- Purchase history and frequency

- Average order values and seasonal patterns

- Customer lifetime value calculations

- Communication preferences and engagement data

- Return and refund patterns

AI-Powered Personalization

Machine learning algorithms process this CRM data to:

- Predict optimal payment schedules based on individual cash flow patterns

- Calculate personalized credit limits using holistic customer profiles

- Identify the best communication cadence for payment reminders

- Suggest upsell opportunities at the right moments in the payment journey

Better Engagement Through Personalization

This isn’t just about making payments more convenient – it’s about creating fundamentally better customer relationships.

For Customers

Reduced financial stress: Payment schedules that align with actual income cycles Higher approval rates: AI considers more factors than traditional credit scoring Flexible adjustments: Plans that adapt to changing circumstances Proactive communication: Reminders and updates delivered when and how customers prefer them

For Businesses

Lower default rates: Payment plans matched to customer capacity reduce missed payments Increased conversion: More customers can afford purchases with personalized terms

Higher customer lifetime value: Better payment experiences drive repeat purchases Improved cash flow predictability: AI helps forecast payment patterns more accurately

The Competitive Advantage

Companies implementing personalized pay paths are seeing impressive results:

- 25-40% reduction in payment defaults compared to generic BNPL

- 15-30% increase in average order values

- Higher customer satisfaction scores and Net Promoter Scores

- Improved operational efficiency through automated, intelligent payment management

What This Means for Your Business

If you’re currently using traditional BNPL solutions, it might be time to evaluate next-generation alternatives. The businesses that will thrive in the evolving payments landscape are those that treat each customer as an individual, not a demographic.

Look for BNPL partners that offer:

- Deep CRM integration capabilities

- AI-driven personalization engines

- Flexible payment structure options

- Advanced analytics and reporting

- White-label customization options

The Future is Personal

We’re moving toward a world where every aspect of the shopping experience adapts to individual preferences and circumstances. Payments are no exception.

The question isn’t whether personalized pay paths will become the standard – it’s how quickly your business will adopt them.

Because in a world where customers have endless choices, the companies that understand them as individuals, not just credit scores, will be the ones that win their loyalty and their wallets.

Why 70%+ CRM Projects Fail…

Why 70%+ CRM Projects Fail — And How Next-Gen Architecture Changes Outcomes January 15, 2026…

Hyper-Personalization as a Competitive Advantage…

Hyper-Personalization as a Competitive Advantage in 2026 January 14, 2026 1:40 pm Adil Gouri Retail…

Salesforce’s Next Frontier: Agentic AI…

Salesforce’s Next Frontier: Agentic AI & Self-Executing Workflows January 14, 2026 11:50 am Darpan Karanje…