Why 70%+ CRM Projects Fail — And How Next-Gen Architecture Changes Outcomes

Why 70%+ CRM Projects Fail — And How Next-Gen Architecture Changes Outcomes January 15, 2026 10:26 am aadinath magar Why 70%+ CRM Projects Fail—and How Architecture Changes Outcomes Most CRM initiatives don’t fail because the platform is weak. They fail quietly, months after go-live, when adoption stalls, data becomes unreliable, and leadership realizes the system hasn’t changed how the business actually operates. The technology works, but the outcomes don’t. That disconnect is why over 70% of CRM projects are labeled “unsuccessful” within two years—not abandoned, but underdelivering on the promise they were meant to fulfill. In large enterprises driving digital transformation, CRM is no longer just a sales or service tool. It sits at the center of revenue operations, customer experience, compliance, analytics, and ecosystem integrations. Expectations are high: real-time visibility, seamless handoffs, AI-driven insights, and scalability across regions and business units. Yet many organizations still implement CRM as a standalone system, disconnected from upstream and downstream processes that actually define enterprise operations. The core problem isn’t configuration—it’s architecture. Traditional CRM implementations focus on objects, screens, and workflows without addressing how data flows across systems, how processes evolve, or how teams actually work at scale. Siloed integrations, point-to-point logic, and excessive customization create brittle systems that are hard to adapt. Over time, CRM becomes something users work around instead of working with. This is where next-generation Salesforce architecture changes the equation. Instead of treating Salesforce as a monolithic system, modern implementations position it as an orchestration layer within a broader digital ecosystem. Using API-led connectivity with MuleSoft, event-driven automation, scalable data models, and governed automation through Flow and platform services, Salesforce becomes resilient by design. The focus shifts from “building features” to enabling adaptable business capabilities. Consider a global enterprise rolling out Salesforce Sales and Service Clouds across multiple regions. Initially, each region customizes heavily to match local processes, resulting in fragmented reporting and inconsistent customer experiences. By re-architecting around shared core objects, standardized automation patterns, and centralized integration services, the organization creates a common operational backbone. Local flexibility still exists, but within a governed, scalable framework. Adoption improves because the system aligns with how teams actually collaborate across geographies. The benefits of this architectural shift are tangible. Data becomes trustworthy because it’s sourced and synchronized correctly. Automation scales without breaking as volumes grow. Enhancements take weeks instead of months because changes don’t cascade unpredictably. Most importantly, CRM starts delivering business outcomes—faster deal cycles, improved service resolution, clearer forecasting—instead of just system usage metrics. Looking ahead, CRM success will be increasingly defined by architectural maturity. As AI-driven insights, real-time analytics, and experience-led ecosystems become standard, enterprises need platforms that can evolve without constant rework. Salesforce’s strength lies not just in features, but in its ability to support composable, future-ready architectures when implemented thoughtfully. If you’re questioning why past CRM investments haven’t delivered expected results, the answer is often less about the tool and more about the foundation beneath it. If you’re evaluating how Salesforce fits into your digital roadmap, we help organizations assess architectural gaps, define scalable implementation strategies, and turn CRM from a system of record into a system of impact. Latest Post 15Jan BlogsTechnology Hyper-Personalization as a Competitive Advantage… Why 70%+ CRM Projects Fail — And How Next-Gen Architecture Changes Outcomes January 15, 2026… 14Jan BlogsTechnology Hyper-Personalization as a Competitive Advantage… Hyper-Personalization as a Competitive Advantage in 2026 January 14, 2026 1:40 pm Adil Gouri Retail… 14Jan BlogsTechnology Salesforce’s Next Frontier: Agentic AI… Salesforce’s Next Frontier: Agentic AI & Self-Executing Workflows January 14, 2026 11:50 am Darpan Karanje…

Hyper-Personalization as a Competitive Advantage in 2026

Hyper-Personalization as a Competitive Advantage in 2026 January 14, 2026 1:40 pm Adil Gouri Retail in 2026: Winning Through Hyper-Personalized Experiences Walk into any retail brand’s ecosystem today—online or offline—and the expectation is already clear. Customers don’t want to be recognized as a segment anymore; they want to be understood as individuals. By 2026, hyper-personalization isn’t a “nice-to-have” experience layer—it’s the baseline customers silently demand, and the differentiator brands quietly compete on. Retail is operating in an environment shaped by fragmented journeys, shrinking loyalty, and relentless comparison. Consumers move fluidly between mobile apps, stores, marketplaces, social platforms, and customer support channels. At the same time, retailers are juggling volatile demand, thin margins, rising acquisition costs, and pressure to convert first-time buyers into long-term advocates. Personalization, once driven by simple recommendation engines, now needs to work in real time, across every touchpoint. The gap today isn’t intent—it’s execution. Many retailers still rely on disconnected systems for commerce, marketing, service, and inventory. Customer data sits in silos, campaign logic is rule-heavy, and personalization often stops at “people like you also bought.” The result is generic experiences powered by complex back-end operations that struggle to scale or adapt quickly to changing customer behavior. This is where Salesforce’s evolution becomes strategically relevant. Salesforce is no longer just a CRM system of record; it’s becoming a system of intelligence. With Salesforce Data Cloud unifying first-party data in real time, Einstein AI interpreting behavior patterns, and tight integration across Commerce Cloud, Marketing Cloud, and Service Cloud, retailers can design experiences that adapt dynamically—without relying on brittle custom logic. Personalization moves from static campaigns to continuous, context-aware decisioning across channels. Consider a mid-sized omnichannel retailer preparing for a peak sales season. Historically, their promotions were calendar-driven and product-focused. By centralizing customer profiles in Data Cloud and applying Einstein-driven insights, they begin tailoring offers based on browsing behavior, store visits, inventory availability, and past service interactions. A customer who abandoned a cart online doesn’t just receive a reminder email—they might see a personalized in-store offer, a relevant product bundle, or proactive service outreach if friction is detected. The experience feels natural, not engineered. Another critical shift retailers are navigating is the balance between personalization and trust. As data volumes grow, customers are becoming more conscious of how their information is collected and used. Hyper-personalization in 2026 will only succeed when it is transparent, compliant, and value-driven. Salesforce’s emphasis on trusted AI, consent-driven data models, and governance through Data Cloud allows retailers to personalize responsibly—delivering relevance without crossing the line into intrusion. Equally important is organizational readiness. Hyper-personalization isn’t powered by technology alone; it requires alignment between marketing, merchandising, service, and IT teams. Salesforce enables this alignment by providing a shared customer language through Customer 360, real-time insights accessible across roles, and automation that reduces dependency on manual handoffs. Retailers that invest in this operational maturity are better positioned to move faster, experiment safely, and scale personalization without adding complexity. The benefits compound quickly. Retailers see higher conversion rates, improved inventory turnover, and stronger customer lifetime value because engagement feels timely and relevant. Operational teams gain clarity instead of complexity, since personalization logic is driven by unified data and AI recommendations rather than manual segmentation and duplicated workflows. Most importantly, trust improves—customers are more willing to share data when the value exchange is obvious. Looking ahead to 2026, hyper-personalization will mature beyond marketing into a full experience ecosystem. AI-driven decisioning, predictive service, autonomous commerce flows, and real-time experience orchestration will define retail leaders. Salesforce’s roadmap aligns closely with this shift, focusing on scalable data foundations, responsible AI, and cross-cloud intelligence that grows with the business—not against it. If you’re evaluating how Salesforce fits into your digital retail roadmap, we help organizations validate personalization strategy, design scalable architectures, and turn CRM investments into measurable, customer-centric outcomes. Latest Post 14Jan BlogsTechnology Hyper-Personalization as a Competitive Advantage… Hyper-Personalization as a Competitive Advantage in 2026 January 14, 2026 1:38 pm Adil Gouri Retail… 14Jan BlogsTechnology Salesforce’s Next Frontier: Agentic AI… Salesforce’s Next Frontier: Agentic AI & Self-Executing Workflows January 14, 2026 11:50 am Darpan Karanje… 14Jan BlogsIndustry Building Real-Time Customer 360 with… Building Real-Time Customer 360 with Salesforce Data Cloud January 14, 2026 11:21 am Laxman Gore…

Salesforce’s Next Frontier: Agentic AI & Self-Executing Workflows

Salesforce’s Next Frontier: Agentic AI & Self-Executing Workflows January 14, 2026 11:50 am Darpan Karanje Turning AI Intelligence into Real-Time Business Impact Most enterprise tech leaders know automation can shave hours off routine work, but what if your systems could think ahead rather than just follow instructions? The conversation is shifting — from task automation to intelligent orchestration that anticipates outcomes, adapts in real-time, and triggers action without human prompts. In an era where generative AI became table stakes, the next battleground is agentic intelligence — AI that autonomously enacts business processes and workflows that traditionally required manual oversight. Technology companies are uniquely pressured to innovate faster, integrate complex stacks, and deliver personalized customer and employee experiences at scale. Yet many still wrestle with operational silos: CRM teams manually escalate support cases, product ops chase cross-cloud handoffs, and sales leaders juggle fragmented views of opportunity risk. Even as workflows grow in complexity, the expectation for real-time execution and insight has never been higher. This intensifies the need for systems that do more than react — systems that act. Despite advancements in low-code automation and Einstein AI insights, a gap persists. Current automation capabilities generally require human orchestration — approvals, triggers, or monitoring to close the loop. Organizations with high-velocity operations still face bottlenecks when transforming insight into action. That’s the core challenge: connecting predictive intelligence with self-directed execution so that meaningful work doesn’t stall at the edge of human intervention. Salesforce is positioning itself at the forefront of this shift by infusing agentic AI into its platform and advancing self-executing workflows. Rather than just suggesting the next best action, agentic capabilities within Salesforce promise context-aware agents that can evaluate priorities, determine the optimal outcome, and execute multi-step processes across clouds — from automating cross-service case routing to initiating contract renewals with contextual approvals. This evolution aligns with Salesforce’s broader strategy of turning intelligence into impact rather than intelligence into recommendations alone. Consider a tech support organization handling high-severity incidents. Today, triggers might alert a manager and create a task for review. With agentic AI and self-executing workflows, the system could automatically assess problem severity, reassign engineers, initiate customer notifications, schedule escalations, and document remediation steps — all without a single manual click. The result is a closed-loop resolution engine that learns from outcomes, improves decision paths, and accelerates time-to-resolution without burdening staff with routine governance tasks. The benefits resonate across performance and culture. Teams waste less time on coordination, leaders gain confidence that high-priority work proceeds reliably, and customers receive faster, more consistent responses. By reducing operational friction, organizations unlock higher innovation capacity — internal talent can focus on strategy and creativity rather than chasing clicks and approvals. The measurable impact includes reduced cycle times, higher SLA compliance, and improved employee satisfaction because the system handles what it can, freeing humans for what only they should. Looking ahead, agentic AI and self-executing workflows are more than feature buzzwords — they represent a new maturity curve in digital operations. As AI models become better at understanding context, intent, and business policies, the frontier will move toward systems that not only respond intelligently but decide and act with bounded autonomy. This evolution will challenge organizations to rethink control frameworks, governance, and trust models — demanding clarity on when and how AI should act on behalf of people and the business. If your organization is evaluating how Salesforce’s emerging AI and automation stack fits into your tech strategy, exploring agentic capabilities and self-executing workflows now can accelerate your path to operational resilience. Aligning human expertise with autonomous execution is no longer a futuristic ideal — it’s becoming a competitive necessity. Latest Post 14Jan BlogsRetail Salesforce’s Next Frontier: Agentic AI… Salesforce’s Next Frontier: Agentic AI & Self-Executing Workflows January 14, 2026 11:49 am Darpan Karanje… 14Jan BlogsIndustry Building Real-Time Customer 360 with… Building Real-Time Customer 360 with Salesforce Data Cloud January 14, 2026 11:21 am Laxman Gore… 19Dec BlogsRetail Why Banks Are Replacing Legacy… Why Banks Are Replacing Legacy CRMs for Omni-Channel Relationship Insight December 19, 2025 11:56 am…

When global disruptions threaten to derail life-saving medical devices, intelligent technology platforms are keeping innovation on track and patients’ hope alive.

MedTech Under Siege: Innovation from Tariffs, Strikes, and Supply Chain Chaos MedTech Under Siege: How Salesforce Rescues Innovation from Tariffs, Strikes, and Supply Chain Chaos October 10, 2025 11:48 am Himakhi Gogoi Your company has a breakthrough medical device ready to change lives. But there’s a problem. New tariffs just made your components 30% more expensive, your supplier can’t guarantee delivery dates, and your support team is down to half its normal size. This isn’t a nightmare scenario. It’s just another Tuesday in medical technology in 2025. The Perfect Storm Hitting Medical Technology Medical technology companies are fighting battles on three fronts simultaneously. Trade wars have made costs unpredictable, with tariffs changing overnight and forcing difficult choices about pricing or finding new suppliers in unfamiliar markets. Global supply chains remain fragile years after pandemic disruptions, with critical components like specialized semiconductors, rare earth materials, and precision-manufactured parts facing extended delays that can push entire product launches back by months. The workforce crisis adds a deeply human dimension to these operational challenges. Major labor actions, exemplified by the 30,000 Kaiser Permanente workers strike, send shockwaves through the healthcare ecosystem. Beyond these visible strikes, medical technology companies struggle daily to find and retain specialized talent in crucial areas like regulatory affairs, clinical research, and technical support. These aren’t positions you can fill quickly with general hires. They require years of specific experience and deep expertise. These challenges create a devastating cascade effect. Delayed components mean missed product launch deadlines. Understaffed customer service teams can’t maintain support quality, damaging relationships with hospitals and clinics. Regulatory submissions slow down because documentation specialists are splitting time across multiple projects instead of focusing on single initiatives. Innovation slows to a crawl precisely when patients need new medical solutions most urgently. Why Innovation Gets Trapped Here’s the frustrating reality that keeps medical technology executives up at night. The industry has never been better positioned to deliver transformative healthcare solutions. Artificial intelligence is enabling earlier disease detection. Connected devices are making remote patient monitoring truly effective. Precision manufacturing is creating implants and prosthetics that work better than ever before. The devices work brilliantly. The clinical data is strong. Patients desperately need these innovations. But operational chaos keeps breakthrough technologies locked in development limbo while external forces beyond anyone’s control dictate timelines and outcomes. Traditional solutions simply aren’t working anymore. Companies tried hiring more people, but specialized talent isn’t available at any reasonable cost. They tried building larger component inventories, but that ties up massive amounts of capital and doesn’t help when tariffs change the economics overnight. They tried diversifying suppliers, but qualifying new vendors for medical-grade components takes months of rigorous validation work. What the industry needs isn’t just more resources or better contingency plans. It needs fundamentally smarter systems that can absorb shocks, adapt quickly to changing conditions, and keep innovation moving forward even when external circumstances are terrible. How Modern Platforms Enable Resilience The medical technology companies thriving despite these challenges share a common characteristic. They’ve invested in integrated technology platforms that give them visibility, control, and flexibility across their entire operation. These aren’t just software tools for managing customer relationships or tracking inventory in spreadsheets. They’re comprehensive ecosystems that connect every part of the business from research and development through manufacturing, regulatory compliance, sales, and customer support into one intelligent system. Think of it like upgrading from a paper map to a real-time GPS navigation system with live traffic updates. When unexpected obstacles appear, the system doesn’t just tell you there’s a problem somewhere ahead. It immediately shows you alternative routes, estimates the impact on your arrival time, and helps you make informed decisions about how to proceed based on current conditions. That’s the kind of operational intelligence medical technology companies need when tariffs hit without warning, suppliers fail to deliver, or workforce challenges emerge suddenly. Where Salesforce Transforms MedTech Operations Salesforce provides medical technology companies with a comprehensive platform that directly tackles each of these challenges while connecting every part of the business into one intelligent, responsive ecosystem. Life Sciences Cloud serves as your operational command center, providing complete visibility across your entire product lifecycle from initial concept through commercialization and beyond. When tariffs hit critical components, the platform immediately flags affected suppliers and products, calculates the financial impact across your portfolio, and enables rapid scenario planning. Product managers can instantly see which development timelines are at risk and reprioritize resources accordingly. Regulatory teams can assess compliance implications across different markets. Sourcing specialists can identify and evaluate alternative suppliers with built-in workflows that track the entire qualification process. Instead of spending weeks gathering information from disconnected systems and endless spreadsheets, companies can respond to major supply chain shocks in days or even hours. Agentforce directly solves the workforce crisis by augmenting stretched human teams with intelligent AI agents that handle substantial portions of routine work across customer service, sales, and internal operations. When a medical device company loses experienced support staff to attrition or labor disputes, Agentforce agents step in seamlessly to handle common technical inquiries, troubleshooting procedures, and product information requests. They work around the clock across multiple languages and channels, providing consistent coverage that would be impossible with human teams alone, especially during workforce shortages. This frees your remaining specialists to focus exclusively on complex cases that truly require human expertise, judgment, and relationship building. On the sales side, these AI agents qualify leads automatically, schedule product demonstrations with healthcare providers, and guide initial product selection conversations. They learn continuously from every interaction, building an ever-growing knowledge base that captures institutional expertise even as individual employees come and go. For medical technology companies struggling with sales team capacity, this means maintaining consistent, professional outreach and responsiveness to potential customers even with skeleton crews. Health Cloud creates the collaboration infrastructure that keeps dispersed, disrupted teams working together effectively despite physical separation or reduced headcount. When workforce shortages mean fewer people trying to accomplish more work, often from different locations due to remote

Digital Lending 2025 (India): Compliant Growth Under RBI’s New Directions

Compliance is the New Growth Hack And Salesforce is Your Engine. Digital Lending 2025 (India): Compliant Growth Under RBI’s New Directions August 20, 2025 10:37 pm Akash Yadav The digital lending landscape in India just got a major overhaul. With RBI issuing the Digital Lending Directions 2025 on May 8, 2025, every digital lender now faces a critical challenge: how do you scale credit operations while staying fully compliant with the most comprehensive regulatory framework India has ever seen? The answer lies not in choosing between growth and compliance, but in redesigning your entire product and platform architecture to make compliance a competitive advantage. The companies that master this integration will dominate the next decade of digital lending in India. The New Reality: Compliance as Core Architecture The 2025 Directions are not just regulatory updates—they represent a fundamental shift in how digital lending must operate. The Chief Compliance Officer (CCO) of each Regulated Entity is now accountable for certifying that all digital lending workflows comply with DLG 2025, making compliance a board-level responsibility that cannot be treated as an afterthought. This means your technology stack, product design, and business processes must be built with compliance at the core, not bolted on as an external layer. The companies that understand this shift early will have a massive advantage over those trying to retrofit compliance into existing systems. Breaking Down the New Framework: What Every Digital Lender Must Know Regulated Entities and Scope The 2025 Directions apply to all commercial banks, primary cooperative banks, state cooperative banks, central cooperative banks, all non-banking financial companies including housing finance companies, and all-India financial institutions. If you are lending digitally in India, these rules apply to you. Default Loss Guarantee: The 5% Cap Revolution The most immediate impact comes from the DLG framework. DLG cover is now capped at 5% of the disbursed portfolio and must be in the form of cash, fixed deposits, or bank guarantees. This fundamentally changes how Lending Service Providers (LSPs) can structure their partnerships with banks and NBFCs. Key implications: No revolving credit or credit card DLGs are permitted DLG must be invoked within 120 days of default unless repaid Once invoked, a guarantee cannot be reinstated For digital lending platforms, this means you need robust systems to: Track DLG utilization in real-time across your portfolio Automate DLG invocation within the 120-day window Maintain separate accounting for different portfolio segments Ensure your underwriting does not rely on DLG as a substitute for proper risk assessment LSP Governance: The New Accountability Framework LSPs can no longer collect fees directly from borrowers; REs must compensate them separately. This creates a complete restructuring of revenue flows in digital lending partnerships. Importantly, LSPs are now under RBI oversight through their contractual arrangements with REs. This means if you are an LSP, your compliance posture directly impacts your banking partners’ regulatory standing. The operational changes required: Complete separation of customer-facing fees from LSP compensation Transparent fee structures that cannot be bundled or hidden Clear contractual frameworks that define compliance responsibilities Joint liability structures between REs and LSPs for regulatory violations CIMS Registration: Your Ticket to Legitimacy All REs must report their Digital Lending Apps on RBI’s CIMS portal by June 15, 2025. The RBI will make this list publicly accessible, allowing users to verify app legitimacy. This is not just a reporting requirement—it is a fundamental shift toward transparency that will reshape customer trust and market dynamics. REs are responsible for the accuracy and timely submission of this information, which will be published by RBI without further validation. The strategic implications: Apps not registered on CIMS will lose customer trust and face regulatory action Public visibility means reputational risks are amplified Accuracy of reporting becomes critical as errors will be publicly visible Chief Compliance Officers must certify the accuracy of DLA data on CIMS portal The Cooling-Off Period: Redefining Customer Experience Borrowers now have a “cooling-off period”, determined by the RE’s board with a minimum of one day, to exit loans without penalties except a nominal processing fee. This seemingly simple requirement creates complex operational challenges. Your platform must now handle: Dynamic cooling-off periods based on different REs’ board decisions Automated loan cancellation processes Refund mechanisms for disbursed amounts Clear communication of cooling-off rights to customers Systems to prevent LSPs from charging fees during this period Key Metrics for Compliant Growth: What to Track To scale successfully under the new framework, you need to monitor compliance metrics alongside business metrics. Here are the critical KPIs: Complaint Rate Metrics Customer complaints per 1000 loans disbursed Resolution time for complaints Complaint categories trending analysis LSP vs direct RE complaint ratios Mis-selling Detection Flags Loan approval to complaint correlation Product complexity vs customer profile mismatches Excessive fee structures detection Inappropriate target customer segments NPA Performance by Channel Direct RE channels vs LSP channel NPA rates DLG invocation frequency by LSP Portfolio performance within the 5% DLG cap Time to default analysis by acquisition channel Approval TAT (Turnaround Time) Compliance End-to-end approval times including cooling-off periods System downtime impact on approval processes Compliance check delays in approval workflows Customer drop-off rates during compliance processes Product and Compliance Co-Design: The Winning Strategy The most successful digital lenders in 2025 will be those that redesign their products with compliance as a core feature, not a constraint. This means: Embedded Compliance Workflows Real-time DLG utilization tracking in loan origination systems Automated cooling-off period management Integrated KYC and customer verification processes Built-in fee transparency and disclosure mechanisms Transparent Pricing Architecture Clear separation of RE fees and LSP compensation Automated fee calculation and disclosure Dynamic pricing based on regulatory requirements Customer-friendly fee explanations and comparisons Risk Management Integration DLG-conscious underwriting models Real-time portfolio monitoring for regulatory limits Automated early warning systems for compliance breaches Integrated stress testing for different regulatory scenarios Platform Changes: Technical Architecture for Compliance Your technology platform needs fundamental changes to support compliant growth: Data Architecture Updates Separate data streams for customer fees and LSP compensation Real-time regulatory reporting capabilities

BNPL is Evolving: What Comes After Pay Later?

Next-Gen FinTech Starts Here BNPL is Evolving: What Comes After Pay Later? BNPL is Evolving: What Comes After Pay Later? August 8, 2025 12:13 pm Kartik Chopade The Buy Now, Pay Later (BNPL) revolution seemed like it happened overnight. One day we were fumbling for credit cards, the next we were splitting purchases into bite-sized installments with a few taps on our phones. But here’s the thing about revolutions – they don’t stop evolving. The BNPL landscape is shifting again, and this time it’s getting personal. Really personal. We’re moving from the one-size-fits-all “pay in 4” model to something far more sophisticated: Personalized Pay Paths. The Problem with Generic BNPL Traditional BNPL solutions treat all customers the same. Whether you’re buying a $50 pair of shoes or a $2,000 laptop, you get the same payment structure. It’s like giving everyone the same prescription glasses – sure, some people might see better, but most are still squinting. This generic approach creates friction for both businesses and customers: High-value purchases often need longer payment terms Repeat customers deserve better flexibility than first-time buyers Different income cycles (weekly, bi-weekly, monthly) require different payment schedules Shopping behavior patterns vary dramatically across customer segments Enter the New Wave: CRM + AI = Smart Payment Journeys The next generation of BNPL platforms is cracking this code by combining two powerful technologies: Customer Relationship Management (CRM) data and Artificial Intelligence. Here’s how it works: Instead of offering everyone the same “4 payments over 6 weeks” option, these smart platforms analyze individual customer data to create tailored payment journeys. They look at purchase history, payment behavior, income patterns, and even seasonal spending habits to craft payment plans that actually make sense for each person. Real-World Example Imagine Sarah, a freelance designer who gets paid monthly, and Mike, a retail worker who gets paid weekly. Traditional BNPL would offer them identical payment schedules. But with personalized pay paths: Sarah gets monthly installments aligned with her freelance payment cycle Mike gets weekly micro-payments that match his paycheck schedule Both get payment amounts optimized for their spending capacity and history The Technology Behind the Magic CRM Integration: The Data Foundation Modern BNPL platforms are integrating deeply with business CRM systems to access rich customer profiles. This includes: Purchase history and frequency Average order values and seasonal patterns Customer lifetime value calculations Communication preferences and engagement data Return and refund patterns AI-Powered Personalization Machine learning algorithms process this CRM data to: Predict optimal payment schedules based on individual cash flow patterns Calculate personalized credit limits using holistic customer profiles Identify the best communication cadence for payment reminders Suggest upsell opportunities at the right moments in the payment journey Better Engagement Through Personalization This isn’t just about making payments more convenient – it’s about creating fundamentally better customer relationships. For Customers Reduced financial stress: Payment schedules that align with actual income cycles Higher approval rates: AI considers more factors than traditional credit scoring Flexible adjustments: Plans that adapt to changing circumstances Proactive communication: Reminders and updates delivered when and how customers prefer them For Businesses Lower default rates: Payment plans matched to customer capacity reduce missed payments Increased conversion: More customers can afford purchases with personalized terms Higher customer lifetime value: Better payment experiences drive repeat purchases Improved cash flow predictability: AI helps forecast payment patterns more accurately The Competitive Advantage Companies implementing personalized pay paths are seeing impressive results: 25-40% reduction in payment defaults compared to generic BNPL 15-30% increase in average order values Higher customer satisfaction scores and Net Promoter Scores Improved operational efficiency through automated, intelligent payment management What This Means for Your Business If you’re currently using traditional BNPL solutions, it might be time to evaluate next-generation alternatives. The businesses that will thrive in the evolving payments landscape are those that treat each customer as an individual, not a demographic. Look for BNPL partners that offer: Deep CRM integration capabilities AI-driven personalization engines Flexible payment structure options Advanced analytics and reporting White-label customization options The Future is Personal We’re moving toward a world where every aspect of the shopping experience adapts to individual preferences and circumstances. Payments are no exception. The question isn’t whether personalized pay paths will become the standard – it’s how quickly your business will adopt them. Because in a world where customers have endless choices, the companies that understand them as individuals, not just credit scores, will be the ones that win their loyalty and their wallets. Latest Post 08Aug Blogs BNPL is Evolving: What Comes… Next-Gen FinTech Starts Here BNPL is Evolving: What Comes After Pay Later? BNPL is Evolving:… 07Aug Blogs The $30 Billion ‘Hidden Profit’… Next-Gen FinTech Starts Here The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How… 07Aug Blogs The Million-Dollar Mistake: Why FinTechs… Next-Gen FinTech Starts Here From Spreadsheet Chaos to Smart CRM: Why FinTechs Can’t Afford to…

The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It

Next-Gen FinTech Starts Here The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It August 7, 2025 2:17 pm Darpan Karanje Picture this: Your fintech company has thousands of customers using your core product, but you’re only capturing a fraction of their potential value. Meanwhile, your competitors are quietly building deeper relationships and higher lifetime values with similar customer bases. The difference? They’ve discovered the hidden profit layer that sits between customer acquisition and churn. This isn’t speculation. Recent industry analysis suggests there’s approximately $30 billion in unrealized revenue sitting dormant across fintech companies worldwide — money that’s hidden in plain sight within existing customer relationships. The key to unlocking it lies in combining behavioral data with intelligent CRM automation to drive strategic cross-selling and maximize customer lifetime value. If you’re a decision-maker in fintech, this represents one of the most significant growth opportunities available today. Here’s how smart companies are capitalizing on it. What Exactly Is This ‘Hidden Profit Layer’? The hidden profit layer refers to the untapped revenue potential within your existing customer base. Most fintech companies excel at acquiring customers for their primary product — whether that’s a payment processor, lending platform, or investment app. But they often miss the goldmine of additional services these same customers would gladly purchase. Consider a typical scenario: A small business signs up for your payment processing solution. They’re happy with the service, but you never discover they also need invoice management, expense tracking, or business loans. Meanwhile, they’re purchasing these services from your competitors, often at higher prices than you could offer. The hidden profit layer emerges when you: Identify cross-sell opportunities early in the customer journey Understand behavioral patterns that indicate readiness to buy Deliver personalized recommendations at the right moment Automate follow-up sequences that nurture interest into purchases Research shows that acquiring a new customer costs 5-25 times more than selling to an existing one. Yet most fintech companies allocate 80% of their resources to acquisition and only 20% to expansion. This imbalance represents massive missed opportunities. How Behavioral Data Reveals Customer Intent Your customers are constantly sending signals about their needs, interests, and purchasing intent. The challenge is recognizing and acting on these signals before competitors do. Behavioral data in fintech context includes: Transaction Patterns: How often customers use your service, average transaction sizes, seasonal variations, and spending categories can reveal unmet needs. A customer processing high-volume B2B payments might need cash flow management tools. Product Usage Depth: Customers who fully utilize your core features are prime candidates for complementary services. Someone maximizing your budgeting tools might be ready for investment products. Support Interactions: The questions customers ask support teams often reveal pain points that additional products could solve. Frequent inquiries about multi-currency support might indicate international expansion needs. Platform Engagement: Time spent in different app sections, feature adoption rates, and content consumption patterns provide insights into customer priorities and interests. External Indicators: Credit score changes, business growth signals, or life events (detected through permissioned data sources) can trigger relevant product recommendations. The magic happens when you analyze these data points collectively rather than in isolation. A customer showing increased transaction volume, exploring advanced features, and asking about integration options is displaying classic expansion signals. The Role of CRM AI in Unlocking Value Traditional CRM systems excel at organizing customer information, but they’re reactive by nature. You enter data, create tasks, and hope your team follows up appropriately. CRM AI transforms this dynamic by making your customer relationship management proactive and predictive. Here’s how AI-powered CRM automation drives results: Predictive Scoring: AI algorithms analyze behavioral patterns to assign expansion scores to each customer. Instead of guessing who might be interested in additional products, you get data-driven prioritization of your best opportunities. Automated Trigger Campaigns: When customers exhibit specific behaviors, AI can automatically initiate personalized outreach sequences. A customer who starts processing international payments might receive targeted information about foreign exchange services. Dynamic Content Personalization: AI customizes email content, app recommendations, and product suggestions based on individual customer profiles and behaviors. This increases relevance and conversion rates significantly. Optimal Timing Intelligence: AI identifies the best times to approach each customer with cross-sell opportunities, maximizing the likelihood of positive responses while avoiding over-communication. Conversation Intelligence: AI can analyze support tickets, sales calls, and customer communications to identify sentiment, extract needs, and recommend next best actions for account managers. The result is a CRM system that doesn’t just store customer information — it actively identifies opportunities and orchestrates the right interactions at the right time. Real-World Impact: The Numbers Don’t Lie Companies implementing AI-driven CRM strategies in fintech are seeing remarkable results: Cross-sell conversion rates increase by 40-60% when recommendations are based on behavioral triggers rather than broad market segments Customer lifetime value grows by an average of 35% within the first year of implementation Time to revenue expansion decreases from months to weeks as automated systems identify and nurture opportunities faster than manual processes Account manager productivity improves by 50% as AI handles routine identification and initial outreach, allowing humans to focus on high-value relationship building One mid-sized payment processor implemented behavioral AI and discovered that customers who used their mobile app more than 10 times per month were 4x more likely to adopt additional financial products. By automatically triggering personalized campaigns for these high-engagement users, they increased their average revenue per customer by 42% in eight months. Implementation Strategy: Where to Start Successfully unlocking your hidden profit layer requires a systematic approach: Phase 1: Data Foundation Start by auditing your current data collection and ensuring you’re capturing meaningful behavioral signals. This might require updating your tracking infrastructure or integrating new data sources. Phase 2: AI Integration Choose CRM AI tools that align with your existing tech stack and can process fintech-specific behavioral patterns. Look for solutions that offer pre-built models for financial services rather than

From Manual to Magical: How FinTech Companies Use Salesforce AI to Transform Collections

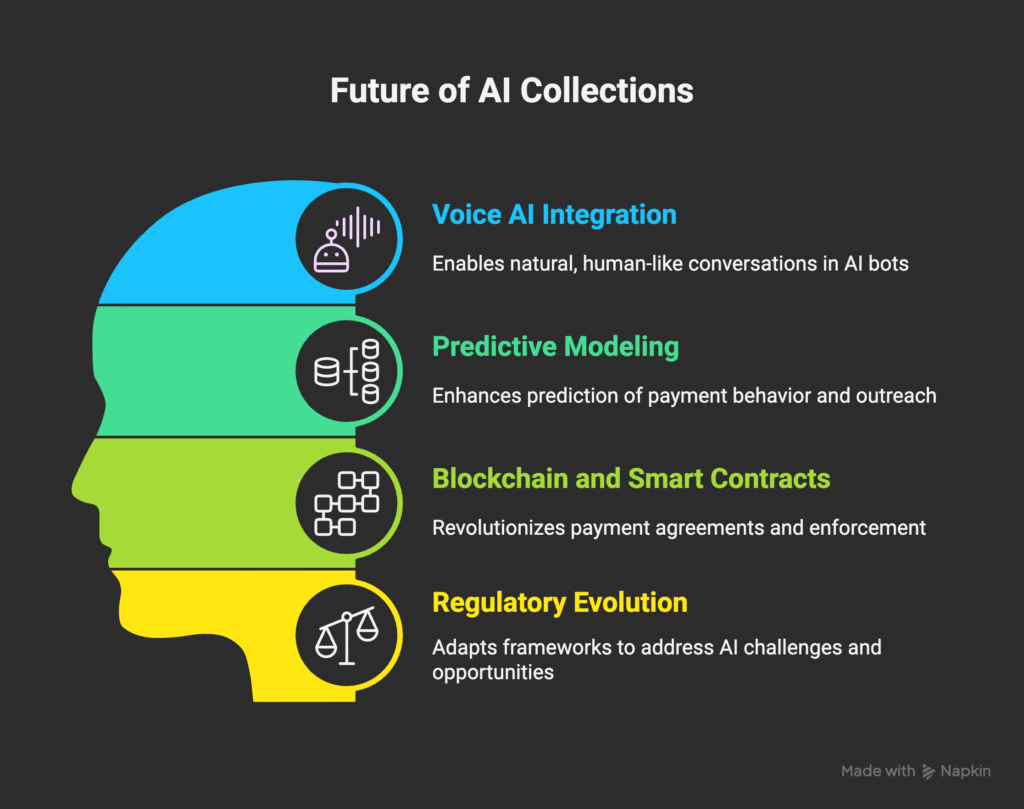

From Manual to Magical: How FinTech Companies Use Salesforce AI to Transform Collections The collections industry is experiencing a seismic shift. While most organizations still rely on human agents making countless phone calls, forward-thinking companies are deploying AI-powered bots that integrate seamlessly with WhatsApp and Salesforce CRM triggers, achieving remarkable cost reductions of up to 40%. The question isn’t whether this transformation will happen—it’s whether your organization will lead or follow. The Current State: Why Manual Collections Are Failing The Human Agent Bottleneck Traditional collections operations are plagued by inefficiencies that seem almost archaic in today’s digital age. Human agents spend hours each day making outbound calls, often reaching voicemails, disconnected numbers, or unresponsive debtors. The average collections agent can only handle 50-80 accounts per day, with success rates hovering around 15-20% for first-contact resolutions. This manual approach creates several critical problems: Scalability Limitations: As portfolios grow, organizations must hire more agents, increasing overhead costs and training complexity. Each new hire requires weeks of training and months to reach full productivity. Inconsistent Messaging: Human agents, despite training, deliver inconsistent messages and may not always follow compliance protocols perfectly. This variability can lead to regulatory issues and damaged customer relationships. Limited Operating Hours: Traditional call centers operate during business hours, missing opportunities to connect with debtors who may only be available during evenings or weekends. High Operational Costs: Between salaries, benefits, training, technology, and facility costs, the total cost per agent can exceed $60,000 annually, not including the productivity losses from sick days, vacation time, and turnover. The Communication Gap Perhaps most critically, traditional collections methods fail to meet modern consumer communication preferences. Studies show that 75% of consumers prefer text-based communication over phone calls, yet most collections operations remain phone-centric. This disconnect creates friction that reduces payment rates and increases customer frustration. The AI Revolution: Transforming Collections Through Intelligent Automation Understanding AI Collections Bots AI collections bots represent a fundamental shift from reactive to proactive collections management. These sophisticated systems leverage natural language processing, machine learning, and integration capabilities to automate the entire collections workflow while maintaining personalization and compliance. Modern AI bots can analyze debtor profiles, payment histories, and behavioral patterns to craft personalized outreach strategies. They understand context, respond to objections, negotiate payment arrangements, and seamlessly escalate complex cases to human agents when necessary. The Power of Multi-Channel Integration The most successful AI collections implementations combine multiple communication channels with robust CRM integration: WhatsApp Business Integration: With over 2 billion users worldwide, WhatsApp has become the preferred communication channel for many consumers. AI bots can initiate conversations, send payment reminders, share payment links, and even process payments directly within the chat interface. Salesforce CRM Triggers: Integration with Salesforce enables sophisticated workflow automation. When specific conditions are met—such as a payment becoming 30 days overdue—the system automatically triggers personalized bot outreach sequences tailored to the debtor’s profile and history. SMS and Email Backup: For comprehensive coverage, AI bots can seamlessly switch between channels based on response rates and customer preferences, ensuring maximum engagement. Real-World Impact: The 40% Cost Reduction Reality Breaking Down the Cost Savings Organizations implementing AI collections bots report average cost reductions of 40%, but understanding where these savings come from reveals the true power of automation: Reduced Labor Costs (60% of savings): AI bots can handle the workload of multiple human agents simultaneously. A single bot can manage thousands of accounts, working 24/7 without breaks, sick days, or vacation time. Increased Collection Rates (25% of savings): By reaching debtors through their preferred communication channels at optimal times, AI bots often achieve higher contact and payment rates than traditional methods. Operational Efficiency (15% of savings): Automated workflows eliminate manual data entry, reduce processing time, and minimize errors, creating significant operational efficiencies. Case Study: Regional Credit Union Success A regional credit union with 50,000 members implemented an AI collections bot integrated with WhatsApp and Salesforce. Within six months, they achieved: 45% reduction in collections operational costs 35% increase in first-contact payment rates 60% reduction in accounts requiring human agent intervention 90% customer satisfaction rate with the bot interaction experience The bot handled over 10,000 collection cases monthly, with human agents focusing only on complex negotiations and legal proceedings. Building Your AI Collections Bot: A Strategic Framework Phase 1: Foundation and Planning Compliance First Approach: Before any technical development, ensure your AI bot framework complies with all relevant regulations including the Fair Debt Collection Practices Act (FDCPA), Telephone Consumer Protection Act (TCPA), and state-specific collection laws. Build compliance into the bot’s core logic, not as an afterthought. Data Integration Strategy: Successful AI collections bots require comprehensive data integration. Connect your existing systems including core banking platforms, loan management systems, payment processors, and customer databases to create a unified view of each debtor’s situation. Communication Channel Setup: Establish your multi-channel communication infrastructure. Set up WhatsApp Business API access, configure SMS gateways, and ensure email deliverability. Each channel requires specific setup and compliance considerations. Phase 2: Salesforce CRM Integration Trigger Configuration: Design sophisticated trigger rules within Salesforce that initiate bot sequences based on specific criteria such as: Days past due thresholds Payment amount and frequency patterns Previous contact history and responses Customer risk scores and segmentation Seasonal or economic factors Workflow Automation: Create automated workflows that update customer records, log interactions, schedule follow-ups, and escalate cases based on bot interactions. This integration ensures seamless handoffs between automated and human processes. Real-Time Sync: Implement real-time data synchronization between your bot platform and Salesforce to ensure agents have immediate access to all bot interactions when they need to intervene. Phase 3: AI Bot Development Natural Language Processing: Develop or integrate NLP capabilities that can understand customer responses, detect payment intent, identify hardship situations, and respond appropriately. The bot should handle common scenarios like payment confirmations, dispute notifications, and arrangement requests. Personalization Engine: Build dynamic message generation capabilities that personalize communications based on customer data, payment history, and previous interactions. Personalized messages consistently outperform generic templates. Payment Integration: Integrate secure payment processing directly