How Salesforce’s Renewable Energy Commitments are Reshaping Corporate Clean Power Procurement

How Salesforce’s Renewable Energy Commitments are Reshaping Corporate Clean Power Procurement November 27, 2025 10:09 am Darpan Karanje Empowering a Sustainable Future: How Salesforce is Driving Innovation and Collaboration in the Global Clean Energy Transition The corporate world is experiencing a fundamental shift in how companies source their electricity. As climate commitments become more than just marketing speak, businesses are discovering that renewable energy procurement is no longer optional. It is essential to competitive advantage, operational resilience, and long-term sustainability. At the forefront of this transformation stands Salesforce, a company that has turned ambitious climate pledges into tangible action. Through innovative procurement strategies, collaborative frameworks, and technology-driven solutions, Salesforce is not just meeting its own renewable energy goals but also reshaping how corporations across industries approach clean power procurement. From Commitment to Action: Salesforce’s Renewable Energy Journey Salesforce made its first public commitment to reach 100% renewable energy in 2013, meaning the company would purchase renewable energy and certificates equivalent to the amount of power used in its global operations every year. What started as a bold promise has evolved into a sophisticated strategy that addresses not just the quantity of renewable energy purchased, but the quality and impact of those purchases. The company recently announced a 15-year virtual power purchase agreement with Qualitas Energy to deliver a new solar portfolio across six Italian regions, expected to generate enough electricity to power over 4,200 homes annually and save over 21,500 metric tons of carbon emissions each year. This marks Salesforce’s first European virtual power purchase agreement, demonstrating how the company is expanding its renewable energy footprint globally while driving real environmental impact. But Salesforce’s approach goes beyond simply buying the cheapest renewable energy available. The company developed a procurement matrix to evaluate renewable energy projects against transactional, economic, environmental and social criteria, recognizing that not all renewable energy is created equal and that two projects with identical transactional details can have enormously different impacts. Breaking Down Barriers Through Collaboration One of Salesforce’s most innovative contributions to corporate renewable energy procurement has been its collaborative approach to solving market barriers. Many companies want to purchase renewable energy but find themselves locked out of favorable procurement options because their energy needs are too small to anchor large renewable energy projects independently. Salesforce addressed this by working with partners to create one of the first examples of companies aggregating similar, relatively small amounts of renewable energy demand to enter into a virtual power purchase agreement collectively, acting as the anchor tenant for a large offsite renewable energy project. Through the Corporate Renewable Energy Aggregation Group, which includes companies like Bloomberg, Cox Enterprises, and Gap Inc., Salesforce demonstrated that smaller buyers can pool their demand and support large-scale projects in the same impactful way larger companies do. This aggregation model has profound implications for the market. It allows companies just starting their renewable energy journey to pilot virtual power purchase agreements as a viable option to meet their climate goals while keeping transaction costs low. More importantly, it creates a blueprint for other corporations to follow, potentially unlocking billions of dollars in renewable energy demand that might otherwise remain untapped. Driving Systemic Change Through Supply Chain Engagement While direct renewable energy procurement addresses a company’s operational emissions, the majority of corporate carbon footprints often lie within supply chains. Salesforce recognized this reality and took decisive action. More than half of Salesforce’s most strategic suppliers have agreed to cut their greenhouse gas emissions as part of binding provisions in their contracts through the Salesforce Sustainability Exhibit, introduced in May 2021, which requires business partners to set science-based emissions reduction targets within two years of signing. This contractual approach represents a significant shift in how corporations can influence emissions beyond their direct operations. Rather than treating sustainability as a nice-to-have feature in vendor selection, Salesforce made it a contractual requirement with real consequences for non-compliance. The initiative is part of Salesforce’s high-level pledge to cut the carbon footprint of its supply chain in half by fiscal year 2031, with the company committed to an absolute reduction of 50 percent for all emissions by 2030. The ripple effects of this approach are substantial. Suppliers who might have delayed setting climate targets are now accelerating their efforts. Some suppliers have even reported that without Salesforce’s requirement, setting targets would have taken significantly longer or might not have happened at all. Investing in the Future of Clean Energy Technology Beyond traditional renewable energy procurement, Salesforce is placing strategic bets on emerging climate technologies that will be essential for reaching net-zero emissions. The company joined Frontier, an advance market commitment to collectively buy more than $1 billion of permanent carbon removal by 2030, committing $25 million to accelerate, scale, and commercialize the most promising carbon removal technologies. This investment in carbon removal solutions reflects a mature understanding of climate action. While reducing emissions should always be the priority, achieving net-zero will ultimately require removing carbon from the atmosphere. By creating demand for carbon removal today, Salesforce is helping these critical technologies scale and become commercially viable. During fiscal year 2024, Salesforce dedicated $10 million to climate justice grants, supporting 18 organizations globally, contributing to the conservation and restoration of over 11,000 hectares of land and catalyzing an estimated $225 million in additional funding. This philanthropic approach recognizes that the energy transition must be equitable and that communities often left behind must be active participants in clean energy solutions. Navigating the Challenges of Rapid Growth As Salesforce continues to expand its business, particularly with the explosive growth of artificial intelligence capabilities, the company faces new challenges in balancing growth with climate commitments. In 2024, the company’s emissions were just 1 percent below its 2018 baseline inventory of roughly 1 million metric tons, and while the company reached its 2030 reduction goals for Scope 1 and 2 two years ago, overall emissions from Scope 3 activities swelled 10 percent between 2019 and 2025. This reality check highlights an important truth: achieving

Digital Platforms + Renewable Asset Management: How Salesforce is Helping Operators Drive Efficiency

Digital Platforms + Renewable Asset Management: How Salesforce is Helping Operators Drive Efficiency November 13, 2025 11:09 am Adil Gouri Empowering a Sustainable Future: Digital Platforms + Renewable Asset Management: How Salesforce is Helping Operators Drive Efficiency The renewable energy sector is experiencing unprecedented growth, with solar farms, wind turbines, and battery storage facilities popping up across the globe. But here’s the challenge: as operators scale their portfolios, managing thousands of distributed assets becomes exponentially complex. The old way of tracking performance, maintenance schedules, and operational data through spreadsheets and disconnected systems simply doesn’t cut it anymore. Enter digital platforms. Today’s renewable energy operators are discovering that the right technology infrastructure can transform how they monitor, maintain, and maximize the performance of their assets. And the results speak for themselves: reduced downtime, optimized maintenance costs, and significantly improved energy output. The Growing Complexity of Renewable Asset Management Managing renewable energy assets isn’t like managing traditional power plants. We’re talking about geographically dispersed installations, each with hundreds or thousands of individual components that need constant monitoring. A single wind farm might have dozens of turbines, each with its own performance profile, maintenance requirements, and potential failure points. The data challenge alone is staggering. Modern renewable installations generate massive amounts of real-time performance data, weather information, grid connection metrics, and maintenance logs. Without a centralized platform to make sense of all this information, operators are essentially flying blind, reacting to problems instead of preventing them. What’s more, today’s energy markets demand agility. Operators need to respond quickly to changing grid conditions, optimize energy delivery based on market prices, and demonstrate performance to investors and stakeholders. Manual processes and siloed data systems make this nearly impossible. How Digital Platforms are Transforming Operations Digital asset management platforms are changing the game by bringing all operational data into a single, intelligent system. Think of it as a command center that gives operators complete visibility into every asset in their portfolio, no matter where it’s located. These platforms connect directly to the sensors and monitoring systems already installed on renewable assets. They collect performance data in real time, analyze it using advanced algorithms, and surface actionable insights that help operators make better decisions faster. When a wind turbine shows early signs of bearing wear, the system flags it immediately. When solar panel performance drops below expected levels, operators know within minutes, not days. The predictive maintenance capabilities are particularly powerful. Instead of scheduling maintenance based on fixed intervals or waiting for equipment to fail, operators can take a data-driven approach. The platform identifies patterns that indicate potential failures, allowing teams to address issues during planned maintenance windows rather than dealing with costly emergency repairs. Beyond maintenance, digital platforms enable portfolio-wide optimization. Operators can compare performance across sites, identify best practices, and replicate success. They can forecast energy production more accurately, helping with grid planning and revenue projections. And when issues do arise, troubleshooting becomes faster because all the relevant data and historical context is immediately available. Real Results: Efficiency Gains in Action The impact of digital platforms on renewable operations is measurable and significant. Operators who have implemented comprehensive asset management platforms report substantial improvements across multiple metrics. Unplanned downtime typically drops by 20 to 30 percent as predictive maintenance catches issues before they become failures. This directly translates to more uptime and higher energy generation. One solar operator found that early detection of inverter issues alone increased their annual production by nearly 3 percent across their portfolio. Maintenance costs also see notable reductions. By shifting from reactive to predictive maintenance, operators avoid expensive emergency repairs and extend equipment lifespan. Technicians spend less time diagnosing problems because the platform has already identified the likely cause, complete with relevant historical data and recommended solutions. Perhaps most importantly, digital platforms improve decision-making at the strategic level. Portfolio managers can quickly assess which assets are underperforming and why, enabling targeted investments in upgrades or optimization. Financial teams get accurate, real-time data for reporting to investors and lenders. And operations teams can allocate resources more effectively, focusing attention where it’s needed most. Breaking Down Data Silos for Better Collaboration One of the less obvious but equally important benefits of digital platforms is how they improve collaboration across teams. In traditional setups, operations teams work in their systems, maintenance crews have their own tools, and finance uses completely different software. Critical information gets trapped in silos, leading to miscommunication and missed opportunities. A unified digital platform breaks down these barriers. Everyone works from the same data source, ensuring alignment across the organization. When a maintenance technician logs work on a turbine, that information is immediately available to operations managers tracking performance and finance teams monitoring costs. Field teams can access the information they need on mobile devices, updating records in real time rather than filing paperwork later. This connected approach also extends to external stakeholders. Asset owners and investors can access customized dashboards showing portfolio performance. Equipment manufacturers can be given secure access to monitor their products and provide proactive support. The entire ecosystem becomes more efficient when everyone has access to accurate, timely information. The Salesforce Advantage in Renewable Energy Operations So where does Salesforce fit into this picture? Many renewable energy operators are discovering that Salesforce’s platform offers exactly the capabilities they need to manage their increasingly complex operations. Salesforce Energy and Utilities Cloud provides a foundation specifically designed for energy sector needs. It connects operational technology with business systems, creating that crucial single source of truth. Asset performance data flows directly into the same platform managing customer relationships, service operations, and business intelligence. The Service Cloud component becomes the backbone of maintenance operations. Work orders are automatically generated based on performance data or scheduled maintenance needs. Field service technicians get mobile access to asset histories, maintenance procedures, and real-time performance metrics. And because everything is connected, resolving issues becomes faster and more efficient. For portfolio management and analytics, Salesforce’s Einstein AI capabilities bring predictive insights to renewable

Digital Lending 2025 (India): Compliant Growth Under RBI’s New Directions

Compliance is the New Growth Hack And Salesforce is Your Engine. Digital Lending 2025 (India): Compliant Growth Under RBI’s New Directions August 20, 2025 10:37 pm Akash Yadav The digital lending landscape in India just got a major overhaul. With RBI issuing the Digital Lending Directions 2025 on May 8, 2025, every digital lender now faces a critical challenge: how do you scale credit operations while staying fully compliant with the most comprehensive regulatory framework India has ever seen? The answer lies not in choosing between growth and compliance, but in redesigning your entire product and platform architecture to make compliance a competitive advantage. The companies that master this integration will dominate the next decade of digital lending in India. The New Reality: Compliance as Core Architecture The 2025 Directions are not just regulatory updates—they represent a fundamental shift in how digital lending must operate. The Chief Compliance Officer (CCO) of each Regulated Entity is now accountable for certifying that all digital lending workflows comply with DLG 2025, making compliance a board-level responsibility that cannot be treated as an afterthought. This means your technology stack, product design, and business processes must be built with compliance at the core, not bolted on as an external layer. The companies that understand this shift early will have a massive advantage over those trying to retrofit compliance into existing systems. Breaking Down the New Framework: What Every Digital Lender Must Know Regulated Entities and Scope The 2025 Directions apply to all commercial banks, primary cooperative banks, state cooperative banks, central cooperative banks, all non-banking financial companies including housing finance companies, and all-India financial institutions. If you are lending digitally in India, these rules apply to you. Default Loss Guarantee: The 5% Cap Revolution The most immediate impact comes from the DLG framework. DLG cover is now capped at 5% of the disbursed portfolio and must be in the form of cash, fixed deposits, or bank guarantees. This fundamentally changes how Lending Service Providers (LSPs) can structure their partnerships with banks and NBFCs. Key implications: No revolving credit or credit card DLGs are permitted DLG must be invoked within 120 days of default unless repaid Once invoked, a guarantee cannot be reinstated For digital lending platforms, this means you need robust systems to: Track DLG utilization in real-time across your portfolio Automate DLG invocation within the 120-day window Maintain separate accounting for different portfolio segments Ensure your underwriting does not rely on DLG as a substitute for proper risk assessment LSP Governance: The New Accountability Framework LSPs can no longer collect fees directly from borrowers; REs must compensate them separately. This creates a complete restructuring of revenue flows in digital lending partnerships. Importantly, LSPs are now under RBI oversight through their contractual arrangements with REs. This means if you are an LSP, your compliance posture directly impacts your banking partners’ regulatory standing. The operational changes required: Complete separation of customer-facing fees from LSP compensation Transparent fee structures that cannot be bundled or hidden Clear contractual frameworks that define compliance responsibilities Joint liability structures between REs and LSPs for regulatory violations CIMS Registration: Your Ticket to Legitimacy All REs must report their Digital Lending Apps on RBI’s CIMS portal by June 15, 2025. The RBI will make this list publicly accessible, allowing users to verify app legitimacy. This is not just a reporting requirement—it is a fundamental shift toward transparency that will reshape customer trust and market dynamics. REs are responsible for the accuracy and timely submission of this information, which will be published by RBI without further validation. The strategic implications: Apps not registered on CIMS will lose customer trust and face regulatory action Public visibility means reputational risks are amplified Accuracy of reporting becomes critical as errors will be publicly visible Chief Compliance Officers must certify the accuracy of DLA data on CIMS portal The Cooling-Off Period: Redefining Customer Experience Borrowers now have a “cooling-off period”, determined by the RE’s board with a minimum of one day, to exit loans without penalties except a nominal processing fee. This seemingly simple requirement creates complex operational challenges. Your platform must now handle: Dynamic cooling-off periods based on different REs’ board decisions Automated loan cancellation processes Refund mechanisms for disbursed amounts Clear communication of cooling-off rights to customers Systems to prevent LSPs from charging fees during this period Key Metrics for Compliant Growth: What to Track To scale successfully under the new framework, you need to monitor compliance metrics alongside business metrics. Here are the critical KPIs: Complaint Rate Metrics Customer complaints per 1000 loans disbursed Resolution time for complaints Complaint categories trending analysis LSP vs direct RE complaint ratios Mis-selling Detection Flags Loan approval to complaint correlation Product complexity vs customer profile mismatches Excessive fee structures detection Inappropriate target customer segments NPA Performance by Channel Direct RE channels vs LSP channel NPA rates DLG invocation frequency by LSP Portfolio performance within the 5% DLG cap Time to default analysis by acquisition channel Approval TAT (Turnaround Time) Compliance End-to-end approval times including cooling-off periods System downtime impact on approval processes Compliance check delays in approval workflows Customer drop-off rates during compliance processes Product and Compliance Co-Design: The Winning Strategy The most successful digital lenders in 2025 will be those that redesign their products with compliance as a core feature, not a constraint. This means: Embedded Compliance Workflows Real-time DLG utilization tracking in loan origination systems Automated cooling-off period management Integrated KYC and customer verification processes Built-in fee transparency and disclosure mechanisms Transparent Pricing Architecture Clear separation of RE fees and LSP compensation Automated fee calculation and disclosure Dynamic pricing based on regulatory requirements Customer-friendly fee explanations and comparisons Risk Management Integration DLG-conscious underwriting models Real-time portfolio monitoring for regulatory limits Automated early warning systems for compliance breaches Integrated stress testing for different regulatory scenarios Platform Changes: Technical Architecture for Compliance Your technology platform needs fundamental changes to support compliant growth: Data Architecture Updates Separate data streams for customer fees and LSP compensation Real-time regulatory reporting capabilities

BNPL is Evolving: What Comes After Pay Later?

Next-Gen FinTech Starts Here BNPL is Evolving: What Comes After Pay Later? BNPL is Evolving: What Comes After Pay Later? August 8, 2025 12:13 pm Kartik Chopade The Buy Now, Pay Later (BNPL) revolution seemed like it happened overnight. One day we were fumbling for credit cards, the next we were splitting purchases into bite-sized installments with a few taps on our phones. But here’s the thing about revolutions – they don’t stop evolving. The BNPL landscape is shifting again, and this time it’s getting personal. Really personal. We’re moving from the one-size-fits-all “pay in 4” model to something far more sophisticated: Personalized Pay Paths. The Problem with Generic BNPL Traditional BNPL solutions treat all customers the same. Whether you’re buying a $50 pair of shoes or a $2,000 laptop, you get the same payment structure. It’s like giving everyone the same prescription glasses – sure, some people might see better, but most are still squinting. This generic approach creates friction for both businesses and customers: High-value purchases often need longer payment terms Repeat customers deserve better flexibility than first-time buyers Different income cycles (weekly, bi-weekly, monthly) require different payment schedules Shopping behavior patterns vary dramatically across customer segments Enter the New Wave: CRM + AI = Smart Payment Journeys The next generation of BNPL platforms is cracking this code by combining two powerful technologies: Customer Relationship Management (CRM) data and Artificial Intelligence. Here’s how it works: Instead of offering everyone the same “4 payments over 6 weeks” option, these smart platforms analyze individual customer data to create tailored payment journeys. They look at purchase history, payment behavior, income patterns, and even seasonal spending habits to craft payment plans that actually make sense for each person. Real-World Example Imagine Sarah, a freelance designer who gets paid monthly, and Mike, a retail worker who gets paid weekly. Traditional BNPL would offer them identical payment schedules. But with personalized pay paths: Sarah gets monthly installments aligned with her freelance payment cycle Mike gets weekly micro-payments that match his paycheck schedule Both get payment amounts optimized for their spending capacity and history The Technology Behind the Magic CRM Integration: The Data Foundation Modern BNPL platforms are integrating deeply with business CRM systems to access rich customer profiles. This includes: Purchase history and frequency Average order values and seasonal patterns Customer lifetime value calculations Communication preferences and engagement data Return and refund patterns AI-Powered Personalization Machine learning algorithms process this CRM data to: Predict optimal payment schedules based on individual cash flow patterns Calculate personalized credit limits using holistic customer profiles Identify the best communication cadence for payment reminders Suggest upsell opportunities at the right moments in the payment journey Better Engagement Through Personalization This isn’t just about making payments more convenient – it’s about creating fundamentally better customer relationships. For Customers Reduced financial stress: Payment schedules that align with actual income cycles Higher approval rates: AI considers more factors than traditional credit scoring Flexible adjustments: Plans that adapt to changing circumstances Proactive communication: Reminders and updates delivered when and how customers prefer them For Businesses Lower default rates: Payment plans matched to customer capacity reduce missed payments Increased conversion: More customers can afford purchases with personalized terms Higher customer lifetime value: Better payment experiences drive repeat purchases Improved cash flow predictability: AI helps forecast payment patterns more accurately The Competitive Advantage Companies implementing personalized pay paths are seeing impressive results: 25-40% reduction in payment defaults compared to generic BNPL 15-30% increase in average order values Higher customer satisfaction scores and Net Promoter Scores Improved operational efficiency through automated, intelligent payment management What This Means for Your Business If you’re currently using traditional BNPL solutions, it might be time to evaluate next-generation alternatives. The businesses that will thrive in the evolving payments landscape are those that treat each customer as an individual, not a demographic. Look for BNPL partners that offer: Deep CRM integration capabilities AI-driven personalization engines Flexible payment structure options Advanced analytics and reporting White-label customization options The Future is Personal We’re moving toward a world where every aspect of the shopping experience adapts to individual preferences and circumstances. Payments are no exception. The question isn’t whether personalized pay paths will become the standard – it’s how quickly your business will adopt them. Because in a world where customers have endless choices, the companies that understand them as individuals, not just credit scores, will be the ones that win their loyalty and their wallets. Latest Post 08Aug Blogs BNPL is Evolving: What Comes… Next-Gen FinTech Starts Here BNPL is Evolving: What Comes After Pay Later? BNPL is Evolving:… 07Aug Blogs The $30 Billion ‘Hidden Profit’… Next-Gen FinTech Starts Here The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How… 07Aug Blogs The Million-Dollar Mistake: Why FinTechs… Next-Gen FinTech Starts Here From Spreadsheet Chaos to Smart CRM: Why FinTechs Can’t Afford to…

The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It

Next-Gen FinTech Starts Here The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It August 7, 2025 2:17 pm Darpan Karanje Picture this: Your fintech company has thousands of customers using your core product, but you’re only capturing a fraction of their potential value. Meanwhile, your competitors are quietly building deeper relationships and higher lifetime values with similar customer bases. The difference? They’ve discovered the hidden profit layer that sits between customer acquisition and churn. This isn’t speculation. Recent industry analysis suggests there’s approximately $30 billion in unrealized revenue sitting dormant across fintech companies worldwide — money that’s hidden in plain sight within existing customer relationships. The key to unlocking it lies in combining behavioral data with intelligent CRM automation to drive strategic cross-selling and maximize customer lifetime value. If you’re a decision-maker in fintech, this represents one of the most significant growth opportunities available today. Here’s how smart companies are capitalizing on it. What Exactly Is This ‘Hidden Profit Layer’? The hidden profit layer refers to the untapped revenue potential within your existing customer base. Most fintech companies excel at acquiring customers for their primary product — whether that’s a payment processor, lending platform, or investment app. But they often miss the goldmine of additional services these same customers would gladly purchase. Consider a typical scenario: A small business signs up for your payment processing solution. They’re happy with the service, but you never discover they also need invoice management, expense tracking, or business loans. Meanwhile, they’re purchasing these services from your competitors, often at higher prices than you could offer. The hidden profit layer emerges when you: Identify cross-sell opportunities early in the customer journey Understand behavioral patterns that indicate readiness to buy Deliver personalized recommendations at the right moment Automate follow-up sequences that nurture interest into purchases Research shows that acquiring a new customer costs 5-25 times more than selling to an existing one. Yet most fintech companies allocate 80% of their resources to acquisition and only 20% to expansion. This imbalance represents massive missed opportunities. How Behavioral Data Reveals Customer Intent Your customers are constantly sending signals about their needs, interests, and purchasing intent. The challenge is recognizing and acting on these signals before competitors do. Behavioral data in fintech context includes: Transaction Patterns: How often customers use your service, average transaction sizes, seasonal variations, and spending categories can reveal unmet needs. A customer processing high-volume B2B payments might need cash flow management tools. Product Usage Depth: Customers who fully utilize your core features are prime candidates for complementary services. Someone maximizing your budgeting tools might be ready for investment products. Support Interactions: The questions customers ask support teams often reveal pain points that additional products could solve. Frequent inquiries about multi-currency support might indicate international expansion needs. Platform Engagement: Time spent in different app sections, feature adoption rates, and content consumption patterns provide insights into customer priorities and interests. External Indicators: Credit score changes, business growth signals, or life events (detected through permissioned data sources) can trigger relevant product recommendations. The magic happens when you analyze these data points collectively rather than in isolation. A customer showing increased transaction volume, exploring advanced features, and asking about integration options is displaying classic expansion signals. The Role of CRM AI in Unlocking Value Traditional CRM systems excel at organizing customer information, but they’re reactive by nature. You enter data, create tasks, and hope your team follows up appropriately. CRM AI transforms this dynamic by making your customer relationship management proactive and predictive. Here’s how AI-powered CRM automation drives results: Predictive Scoring: AI algorithms analyze behavioral patterns to assign expansion scores to each customer. Instead of guessing who might be interested in additional products, you get data-driven prioritization of your best opportunities. Automated Trigger Campaigns: When customers exhibit specific behaviors, AI can automatically initiate personalized outreach sequences. A customer who starts processing international payments might receive targeted information about foreign exchange services. Dynamic Content Personalization: AI customizes email content, app recommendations, and product suggestions based on individual customer profiles and behaviors. This increases relevance and conversion rates significantly. Optimal Timing Intelligence: AI identifies the best times to approach each customer with cross-sell opportunities, maximizing the likelihood of positive responses while avoiding over-communication. Conversation Intelligence: AI can analyze support tickets, sales calls, and customer communications to identify sentiment, extract needs, and recommend next best actions for account managers. The result is a CRM system that doesn’t just store customer information — it actively identifies opportunities and orchestrates the right interactions at the right time. Real-World Impact: The Numbers Don’t Lie Companies implementing AI-driven CRM strategies in fintech are seeing remarkable results: Cross-sell conversion rates increase by 40-60% when recommendations are based on behavioral triggers rather than broad market segments Customer lifetime value grows by an average of 35% within the first year of implementation Time to revenue expansion decreases from months to weeks as automated systems identify and nurture opportunities faster than manual processes Account manager productivity improves by 50% as AI handles routine identification and initial outreach, allowing humans to focus on high-value relationship building One mid-sized payment processor implemented behavioral AI and discovered that customers who used their mobile app more than 10 times per month were 4x more likely to adopt additional financial products. By automatically triggering personalized campaigns for these high-engagement users, they increased their average revenue per customer by 42% in eight months. Implementation Strategy: Where to Start Successfully unlocking your hidden profit layer requires a systematic approach: Phase 1: Data Foundation Start by auditing your current data collection and ensuring you’re capturing meaningful behavioral signals. This might require updating your tracking infrastructure or integrating new data sources. Phase 2: AI Integration Choose CRM AI tools that align with your existing tech stack and can process fintech-specific behavioral patterns. Look for solutions that offer pre-built models for financial services rather than

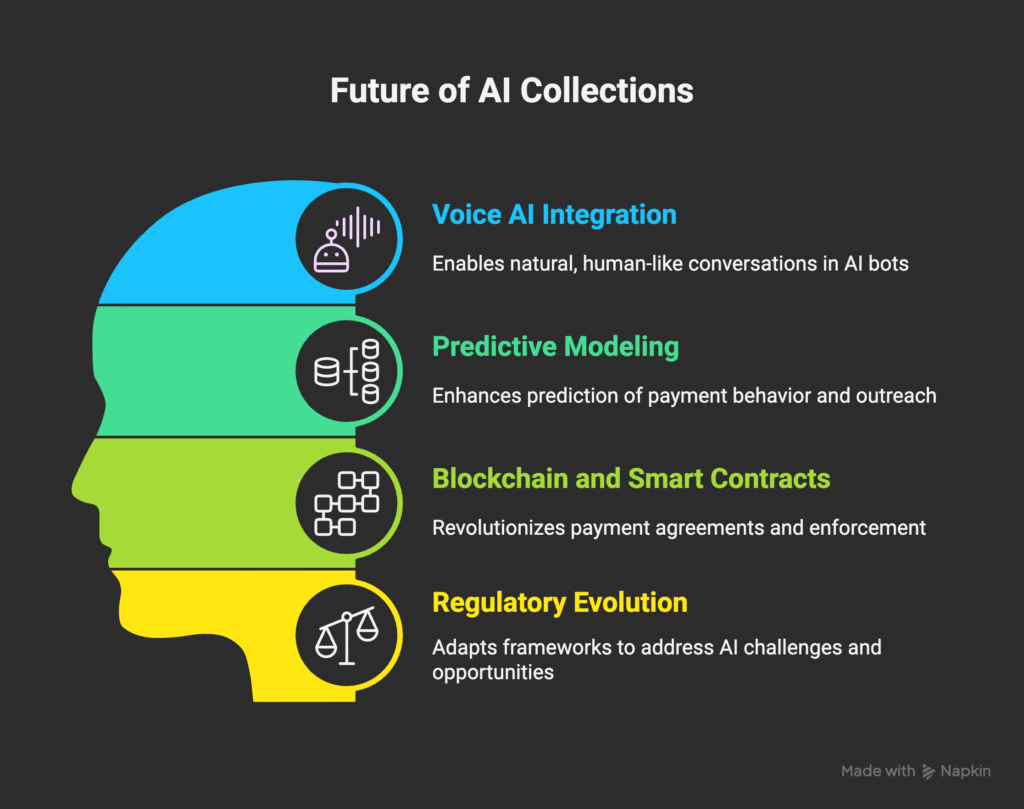

From Manual to Magical: How FinTech Companies Use Salesforce AI to Transform Collections

From Manual to Magical: How FinTech Companies Use Salesforce AI to Transform Collections The collections industry is experiencing a seismic shift. While most organizations still rely on human agents making countless phone calls, forward-thinking companies are deploying AI-powered bots that integrate seamlessly with WhatsApp and Salesforce CRM triggers, achieving remarkable cost reductions of up to 40%. The question isn’t whether this transformation will happen—it’s whether your organization will lead or follow. The Current State: Why Manual Collections Are Failing The Human Agent Bottleneck Traditional collections operations are plagued by inefficiencies that seem almost archaic in today’s digital age. Human agents spend hours each day making outbound calls, often reaching voicemails, disconnected numbers, or unresponsive debtors. The average collections agent can only handle 50-80 accounts per day, with success rates hovering around 15-20% for first-contact resolutions. This manual approach creates several critical problems: Scalability Limitations: As portfolios grow, organizations must hire more agents, increasing overhead costs and training complexity. Each new hire requires weeks of training and months to reach full productivity. Inconsistent Messaging: Human agents, despite training, deliver inconsistent messages and may not always follow compliance protocols perfectly. This variability can lead to regulatory issues and damaged customer relationships. Limited Operating Hours: Traditional call centers operate during business hours, missing opportunities to connect with debtors who may only be available during evenings or weekends. High Operational Costs: Between salaries, benefits, training, technology, and facility costs, the total cost per agent can exceed $60,000 annually, not including the productivity losses from sick days, vacation time, and turnover. The Communication Gap Perhaps most critically, traditional collections methods fail to meet modern consumer communication preferences. Studies show that 75% of consumers prefer text-based communication over phone calls, yet most collections operations remain phone-centric. This disconnect creates friction that reduces payment rates and increases customer frustration. The AI Revolution: Transforming Collections Through Intelligent Automation Understanding AI Collections Bots AI collections bots represent a fundamental shift from reactive to proactive collections management. These sophisticated systems leverage natural language processing, machine learning, and integration capabilities to automate the entire collections workflow while maintaining personalization and compliance. Modern AI bots can analyze debtor profiles, payment histories, and behavioral patterns to craft personalized outreach strategies. They understand context, respond to objections, negotiate payment arrangements, and seamlessly escalate complex cases to human agents when necessary. The Power of Multi-Channel Integration The most successful AI collections implementations combine multiple communication channels with robust CRM integration: WhatsApp Business Integration: With over 2 billion users worldwide, WhatsApp has become the preferred communication channel for many consumers. AI bots can initiate conversations, send payment reminders, share payment links, and even process payments directly within the chat interface. Salesforce CRM Triggers: Integration with Salesforce enables sophisticated workflow automation. When specific conditions are met—such as a payment becoming 30 days overdue—the system automatically triggers personalized bot outreach sequences tailored to the debtor’s profile and history. SMS and Email Backup: For comprehensive coverage, AI bots can seamlessly switch between channels based on response rates and customer preferences, ensuring maximum engagement. Real-World Impact: The 40% Cost Reduction Reality Breaking Down the Cost Savings Organizations implementing AI collections bots report average cost reductions of 40%, but understanding where these savings come from reveals the true power of automation: Reduced Labor Costs (60% of savings): AI bots can handle the workload of multiple human agents simultaneously. A single bot can manage thousands of accounts, working 24/7 without breaks, sick days, or vacation time. Increased Collection Rates (25% of savings): By reaching debtors through their preferred communication channels at optimal times, AI bots often achieve higher contact and payment rates than traditional methods. Operational Efficiency (15% of savings): Automated workflows eliminate manual data entry, reduce processing time, and minimize errors, creating significant operational efficiencies. Case Study: Regional Credit Union Success A regional credit union with 50,000 members implemented an AI collections bot integrated with WhatsApp and Salesforce. Within six months, they achieved: 45% reduction in collections operational costs 35% increase in first-contact payment rates 60% reduction in accounts requiring human agent intervention 90% customer satisfaction rate with the bot interaction experience The bot handled over 10,000 collection cases monthly, with human agents focusing only on complex negotiations and legal proceedings. Building Your AI Collections Bot: A Strategic Framework Phase 1: Foundation and Planning Compliance First Approach: Before any technical development, ensure your AI bot framework complies with all relevant regulations including the Fair Debt Collection Practices Act (FDCPA), Telephone Consumer Protection Act (TCPA), and state-specific collection laws. Build compliance into the bot’s core logic, not as an afterthought. Data Integration Strategy: Successful AI collections bots require comprehensive data integration. Connect your existing systems including core banking platforms, loan management systems, payment processors, and customer databases to create a unified view of each debtor’s situation. Communication Channel Setup: Establish your multi-channel communication infrastructure. Set up WhatsApp Business API access, configure SMS gateways, and ensure email deliverability. Each channel requires specific setup and compliance considerations. Phase 2: Salesforce CRM Integration Trigger Configuration: Design sophisticated trigger rules within Salesforce that initiate bot sequences based on specific criteria such as: Days past due thresholds Payment amount and frequency patterns Previous contact history and responses Customer risk scores and segmentation Seasonal or economic factors Workflow Automation: Create automated workflows that update customer records, log interactions, schedule follow-ups, and escalate cases based on bot interactions. This integration ensures seamless handoffs between automated and human processes. Real-Time Sync: Implement real-time data synchronization between your bot platform and Salesforce to ensure agents have immediate access to all bot interactions when they need to intervene. Phase 3: AI Bot Development Natural Language Processing: Develop or integrate NLP capabilities that can understand customer responses, detect payment intent, identify hardship situations, and respond appropriately. The bot should handle common scenarios like payment confirmations, dispute notifications, and arrangement requests. Personalization Engine: Build dynamic message generation capabilities that personalize communications based on customer data, payment history, and previous interactions. Personalized messages consistently outperform generic templates. Payment Integration: Integrate secure payment processing directly

Salesforce Marketing Account Engagement

Unlocking B2B Marketing Success with Salesforce Marketing Account Engagement In today’s competitive B2B landscape, marketing teams need sophisticated tools to nurture leads, align with sales, and drive revenue growth. Salesforce Marketing Account Engagement (formerly known as Pardot) has emerged as a game-changing solution that transforms how businesses approach account-based marketing and lead nurturing. What is Salesforce Marketing Account Engagement? Salesforce Marketing Account Engagement is a comprehensive B2B marketing automation platform designed to help businesses generate more qualified leads, accelerate sales cycles, and maximize marketing ROI. As part of the Salesforce ecosystem, it seamlessly integrates with Sales Cloud, providing a unified view of prospects and customers throughout their entire journey. The platform empowers marketing teams to create personalized experiences at scale, automate repetitive tasks, and deliver the right message to the right prospect at the right time. Whether you’re targeting individual leads or entire buying committees, Marketing Account Engagement provides the tools needed to orchestrate sophisticated marketing campaigns. Key Features That Drive Results Lead Scoring and Grading- One of the platform’s most powerful features is its dual approach to lead qualification. Lead scoring measures engagement levels based on actions like email opens, website visits, and content downloads. Lead grading evaluates how well a prospect fits your ideal customer profile based on demographic and firmographic data. This combination helps sales teams prioritize their efforts on the most promising opportunities. Dynamic Content and Personalization- Marketing Account Engagement enables marketers to create highly personalized experiences without creating dozens of separate campaigns. Dynamic content adjusts based on prospect attributes, behavior, and engagement history, ensuring every interaction feels relevant and valuable. Advanced Email Marketing- The platform offers sophisticated email marketing capabilities, including A/B testing, responsive templates, and automated drip campaigns. Marketers can create complex email workflows that adapt based on prospect behavior, ensuring optimal engagement throughout the customer journey. Account-Based Marketing (ABM)- With built-in ABM capabilities, Marketing Account Engagement helps teams identify and target high-value accounts. The platform provides account-level insights, enables coordinated campaigns across multiple contacts within target accounts, and offers specialized reporting to measure ABM success. The Power of Salesforce Integratio What sets Marketing Account Engagement apart is its native integration with Salesforce CRM. This connection creates a seamless flow of information between marketing and sales teams, enabling: Unified Lead Management: Prospects automatically sync between systems, ensuring both teams work with the same, up-to-date information. Closed-Loop Reporting: Marketers can track the complete customer journey from first touch to closed deal, providing clear visibility into marketing’s impact on revenue. Sales Enablement: Sales teams receive rich prospect insights, including engagement history, content consumption, and behavioral triggers, enabling more informed conversations. Real-World Applications Lead Nurturing Campaigns- A typical nurturing campaign might begin when a prospect downloads a white paper. Marketing Account Engagement can automatically enroll them in a series of educational emails, track their engagement, and trigger alerts when they show buying signals. If the prospect visits your pricing page multiple times, the system can automatically notify sales for timely follow-up. Event Marketing- For companies that rely on events and webinars, Marketing Account Engagement streamlines the entire process. From registration landing pages to automated follow-up sequences, the platform ensures no lead falls through the cracks. Post-event nurturing campaigns can be triggered based on attendance, engagement level, or specific sessions attended. Content Marketing Optimization- The platform tracks how prospects interact with your content, revealing which pieces drive the most engagement and conversions. This data helps marketers refine their content strategy and create more effective campaigns. Measuring Success Marketing Account Engagement provides comprehensive analytics that go beyond basic email metrics. Key performance indicators include: Pipeline velocity: How quickly leads move through the sales funnel Marketing qualified leads (MQLs): Prospects who meet defined criteria for sales readiness Return on investment: Direct correlation between marketing activities and revenue Account engagement: Comprehensive view of how entire buying committees interact with your brand Best Practices for Implementation Successful Marketing Account Engagement implementation requires careful planning and ongoing optimization. Start by defining clear lead scoring criteria based on your ideal customer profile and typical buying journey. Establish service level agreements between marketing and sales teams to ensure smooth lead handoffs. Content mapping is crucial for effective nurturing campaigns. Align your content with different stages of the buyer’s journey and create automated workflows that deliver the right content at the right time. Regular testing and optimization ensure your campaigns continue to improve performance over time. The Future of B2B Marketing As B2B buying processes become more complex and involve larger committees, platforms like Marketing Account Engagement become increasingly valuable. The ability to orchestrate personalized experiences across multiple touchpoints while maintaining visibility into the entire customer journey is essential for modern marketing success. Organizations that leverage Marketing Account Engagement effectively often see significant improvements in lead quality, sales conversion rates, and overall marketing efficiency. The platform’s AI-powered insights and automation capabilities free up marketers to focus on strategy and creativity rather than manual tasks.