Digital Platforms + Renewable Asset Management: How Salesforce is Helping Operators Drive Efficiency

Digital Platforms + Renewable Asset Management: How Salesforce is Helping Operators Drive Efficiency November 13, 2025 11:09 am Adil Gouri Empowering a Sustainable Future: Digital Platforms + Renewable Asset Management: How Salesforce is Helping Operators Drive Efficiency The renewable energy sector is experiencing unprecedented growth, with solar farms, wind turbines, and battery storage facilities popping up across the globe. But here’s the challenge: as operators scale their portfolios, managing thousands of distributed assets becomes exponentially complex. The old way of tracking performance, maintenance schedules, and operational data through spreadsheets and disconnected systems simply doesn’t cut it anymore. Enter digital platforms. Today’s renewable energy operators are discovering that the right technology infrastructure can transform how they monitor, maintain, and maximize the performance of their assets. And the results speak for themselves: reduced downtime, optimized maintenance costs, and significantly improved energy output. The Growing Complexity of Renewable Asset Management Managing renewable energy assets isn’t like managing traditional power plants. We’re talking about geographically dispersed installations, each with hundreds or thousands of individual components that need constant monitoring. A single wind farm might have dozens of turbines, each with its own performance profile, maintenance requirements, and potential failure points. The data challenge alone is staggering. Modern renewable installations generate massive amounts of real-time performance data, weather information, grid connection metrics, and maintenance logs. Without a centralized platform to make sense of all this information, operators are essentially flying blind, reacting to problems instead of preventing them. What’s more, today’s energy markets demand agility. Operators need to respond quickly to changing grid conditions, optimize energy delivery based on market prices, and demonstrate performance to investors and stakeholders. Manual processes and siloed data systems make this nearly impossible. How Digital Platforms are Transforming Operations Digital asset management platforms are changing the game by bringing all operational data into a single, intelligent system. Think of it as a command center that gives operators complete visibility into every asset in their portfolio, no matter where it’s located. These platforms connect directly to the sensors and monitoring systems already installed on renewable assets. They collect performance data in real time, analyze it using advanced algorithms, and surface actionable insights that help operators make better decisions faster. When a wind turbine shows early signs of bearing wear, the system flags it immediately. When solar panel performance drops below expected levels, operators know within minutes, not days. The predictive maintenance capabilities are particularly powerful. Instead of scheduling maintenance based on fixed intervals or waiting for equipment to fail, operators can take a data-driven approach. The platform identifies patterns that indicate potential failures, allowing teams to address issues during planned maintenance windows rather than dealing with costly emergency repairs. Beyond maintenance, digital platforms enable portfolio-wide optimization. Operators can compare performance across sites, identify best practices, and replicate success. They can forecast energy production more accurately, helping with grid planning and revenue projections. And when issues do arise, troubleshooting becomes faster because all the relevant data and historical context is immediately available. Real Results: Efficiency Gains in Action The impact of digital platforms on renewable operations is measurable and significant. Operators who have implemented comprehensive asset management platforms report substantial improvements across multiple metrics. Unplanned downtime typically drops by 20 to 30 percent as predictive maintenance catches issues before they become failures. This directly translates to more uptime and higher energy generation. One solar operator found that early detection of inverter issues alone increased their annual production by nearly 3 percent across their portfolio. Maintenance costs also see notable reductions. By shifting from reactive to predictive maintenance, operators avoid expensive emergency repairs and extend equipment lifespan. Technicians spend less time diagnosing problems because the platform has already identified the likely cause, complete with relevant historical data and recommended solutions. Perhaps most importantly, digital platforms improve decision-making at the strategic level. Portfolio managers can quickly assess which assets are underperforming and why, enabling targeted investments in upgrades or optimization. Financial teams get accurate, real-time data for reporting to investors and lenders. And operations teams can allocate resources more effectively, focusing attention where it’s needed most. Breaking Down Data Silos for Better Collaboration One of the less obvious but equally important benefits of digital platforms is how they improve collaboration across teams. In traditional setups, operations teams work in their systems, maintenance crews have their own tools, and finance uses completely different software. Critical information gets trapped in silos, leading to miscommunication and missed opportunities. A unified digital platform breaks down these barriers. Everyone works from the same data source, ensuring alignment across the organization. When a maintenance technician logs work on a turbine, that information is immediately available to operations managers tracking performance and finance teams monitoring costs. Field teams can access the information they need on mobile devices, updating records in real time rather than filing paperwork later. This connected approach also extends to external stakeholders. Asset owners and investors can access customized dashboards showing portfolio performance. Equipment manufacturers can be given secure access to monitor their products and provide proactive support. The entire ecosystem becomes more efficient when everyone has access to accurate, timely information. The Salesforce Advantage in Renewable Energy Operations So where does Salesforce fit into this picture? Many renewable energy operators are discovering that Salesforce’s platform offers exactly the capabilities they need to manage their increasingly complex operations. Salesforce Energy and Utilities Cloud provides a foundation specifically designed for energy sector needs. It connects operational technology with business systems, creating that crucial single source of truth. Asset performance data flows directly into the same platform managing customer relationships, service operations, and business intelligence. The Service Cloud component becomes the backbone of maintenance operations. Work orders are automatically generated based on performance data or scheduled maintenance needs. Field service technicians get mobile access to asset histories, maintenance procedures, and real-time performance metrics. And because everything is connected, resolving issues becomes faster and more efficient. For portfolio management and analytics, Salesforce’s Einstein AI capabilities bring predictive insights to renewable

From Fragmented Systems to Unified Care: How Smart Integration Is Turning Healthcare’s AI Challenges Into a Multi-Billion Dollar Success Story

AI Revolution Stalled? How Salesforce Supercharges Healthcare’s Digital Leap to $419B Glory AI Revolution Stalled? How Salesforce Supercharges Healthcare’s Digital Leap to $419B Glory October 17, 2025 1:23 pm Himakhi Gogoi The healthcare industry stands at a crossroads. While artificial intelligence promised to transform patient care overnight, many organizations are discovering that adoption is messier than the headlines suggested. Yet amid the growing pains, there’s a $419 billion opportunity taking shape, and the companies getting it right are the ones combining smart technology with practical implementation strategies. If you’re a healthcare executive or IT decision-maker watching your AI investments plateau while competitors seem to be racing ahead, you’re not alone. The good news? The path forward is clearer than you think, and it starts with understanding why the revolution hit the brakes in the first place. The Promise vs. The Reality of Healthcare AI Healthcare was supposed to be AI’s poster child. Predictive diagnostics, personalized treatment plans, automated administrative workflows—the vision was compelling. Organizations invested heavily, expecting rapid transformation. But here’s what actually happened. Most healthcare systems found themselves drowning in disconnected data sources. Patient information lived in one system, billing in another, clinical notes somewhere else entirely. AI models are only as good as the data they’re trained on, and fragmented information creates fragmented results. The initial excitement gave way to frustration. Pilot programs showed promise but struggled to scale. Clinical staff resisted tools that didn’t fit their workflows. Regulatory concerns slowed deployment. The AI revolution didn’t stall because the technology failed. It stalled because implementation was harder than anyone anticipated. Why Healthcare Needs More Than Just AI The healthcare digital transformation market is projected to reach $419 billion, but capturing that value requires more than deploying algorithms. It demands a fundamental rethinking of how technology integrates with care delivery. Think about what healthcare organizations actually need. They need systems that talk to each other seamlessly. They need insights that clinicians can act on immediately, not data they have to interpret. They need tools that reduce administrative burden rather than adding complexity. Most importantly, they need technology that enhances the patient experience while supporting better outcomes. This is where many AI initiatives miss the mark. A brilliant predictive model means nothing if doctors can’t access its insights during patient consultations. An automated scheduling system fails if it doesn’t connect with insurance verification and medical records. The technology has to work within the existing ecosystem, not apart from it. The Data Integration Challenge Nobody Talks About Behind every successful healthcare AI implementation is an unglamorous truth: data integration is the real battleground. Healthcare organizations accumulate information from dozens of sources including electronic health records, imaging systems, laboratory information systems, billing platforms, and increasingly, patient-generated data from wearables and apps. Getting all this information to work together isn’t just a technical challenge. It’s an organizational one. Different departments have different priorities. Legacy systems weren’t built to communicate. Privacy regulations add layers of complexity. And throughout it all, patient care can’t stop while you rebuild the infrastructure. The organizations making progress aren’t necessarily the ones with the most advanced AI. They’re the ones who solved the data problem first. They created unified patient views. They broke down information silos. They built systems where insights flow naturally to the people who need them, when they need them. Where the $419B Opportunity Actually Lives So where is all that value hiding? It’s not in flashy consumer apps or futuristic robot surgeons, though those make better headlines. The real opportunity lies in three core areas that directly impact healthcare’s bottom line and patient outcomes. First, operational efficiency. Healthcare organizations waste enormous resources on administrative tasks, redundant processes, and coordination failures. Technology that streamlines these operations while maintaining care quality delivers immediate ROI. We’re talking about intelligent scheduling that reduces no-shows, automated prior authorizations that save staff hours, and supply chain optimization that cuts costs without compromising care. Second, clinical decision support. Physicians make thousands of decisions daily, often under time pressure with incomplete information. Systems that surface the right insights at the right moment enhance clinical judgment without replacing it. This means flagging potential drug interactions, identifying patients at risk for readmission, or suggesting evidence-based treatment protocols tailored to individual patient characteristics. Third, patient engagement and experience. Healthcare is finally recognizing that patient satisfaction isn’t just nice to have, it’s essential. Digital tools that improve communication, simplify access to care, and empower patients to manage their health create value for everyone. Better engagement leads to better adherence, better outcomes, and better financial performance. How Salesforce Turns Healthcare’s Digital Challenges Into Competitive Advantages This is where platform thinking changes the game. Healthcare organizations don’t need more disconnected point solutions. They need an integrated ecosystem that brings everything together, and Salesforce Health Cloud is purpose-built for exactly this challenge. Salesforce addresses the core problems holding healthcare AI back. Its platform creates a unified view of each patient by connecting data from multiple sources into a single, comprehensive record. Clinical teams see complete patient histories, upcoming appointments, care plans, and communication logs all in one place. This isn’t just convenient, it’s transformative for care coordination. The platform’s AI capabilities, powered by Einstein, work within this integrated environment. That means predictive insights aren’t isolated reports, they’re embedded directly into clinical and administrative workflows. A care coordinator sees which patients are at risk for readmission right within their daily dashboard. Scheduling systems automatically optimize appointment times based on predicted no-show probability and patient preferences. What makes this approach powerful is that it scales. Healthcare organizations can start with specific use cases like patient engagement or care coordination and expand systematically. The underlying platform handles the complex integration work, so teams can focus on improving care delivery rather than wrestling with technical infrastructure. Salesforce also addresses the collaboration challenge that derails so many digital initiatives. Its tools are designed for how healthcare teams actually work, supporting communication between providers, patients, and administrative staff. When everyone operates from the same information

When global disruptions threaten to derail life-saving medical devices, intelligent technology platforms are keeping innovation on track and patients’ hope alive.

MedTech Under Siege: Innovation from Tariffs, Strikes, and Supply Chain Chaos MedTech Under Siege: How Salesforce Rescues Innovation from Tariffs, Strikes, and Supply Chain Chaos October 10, 2025 11:48 am Himakhi Gogoi Your company has a breakthrough medical device ready to change lives. But there’s a problem. New tariffs just made your components 30% more expensive, your supplier can’t guarantee delivery dates, and your support team is down to half its normal size. This isn’t a nightmare scenario. It’s just another Tuesday in medical technology in 2025. The Perfect Storm Hitting Medical Technology Medical technology companies are fighting battles on three fronts simultaneously. Trade wars have made costs unpredictable, with tariffs changing overnight and forcing difficult choices about pricing or finding new suppliers in unfamiliar markets. Global supply chains remain fragile years after pandemic disruptions, with critical components like specialized semiconductors, rare earth materials, and precision-manufactured parts facing extended delays that can push entire product launches back by months. The workforce crisis adds a deeply human dimension to these operational challenges. Major labor actions, exemplified by the 30,000 Kaiser Permanente workers strike, send shockwaves through the healthcare ecosystem. Beyond these visible strikes, medical technology companies struggle daily to find and retain specialized talent in crucial areas like regulatory affairs, clinical research, and technical support. These aren’t positions you can fill quickly with general hires. They require years of specific experience and deep expertise. These challenges create a devastating cascade effect. Delayed components mean missed product launch deadlines. Understaffed customer service teams can’t maintain support quality, damaging relationships with hospitals and clinics. Regulatory submissions slow down because documentation specialists are splitting time across multiple projects instead of focusing on single initiatives. Innovation slows to a crawl precisely when patients need new medical solutions most urgently. Why Innovation Gets Trapped Here’s the frustrating reality that keeps medical technology executives up at night. The industry has never been better positioned to deliver transformative healthcare solutions. Artificial intelligence is enabling earlier disease detection. Connected devices are making remote patient monitoring truly effective. Precision manufacturing is creating implants and prosthetics that work better than ever before. The devices work brilliantly. The clinical data is strong. Patients desperately need these innovations. But operational chaos keeps breakthrough technologies locked in development limbo while external forces beyond anyone’s control dictate timelines and outcomes. Traditional solutions simply aren’t working anymore. Companies tried hiring more people, but specialized talent isn’t available at any reasonable cost. They tried building larger component inventories, but that ties up massive amounts of capital and doesn’t help when tariffs change the economics overnight. They tried diversifying suppliers, but qualifying new vendors for medical-grade components takes months of rigorous validation work. What the industry needs isn’t just more resources or better contingency plans. It needs fundamentally smarter systems that can absorb shocks, adapt quickly to changing conditions, and keep innovation moving forward even when external circumstances are terrible. How Modern Platforms Enable Resilience The medical technology companies thriving despite these challenges share a common characteristic. They’ve invested in integrated technology platforms that give them visibility, control, and flexibility across their entire operation. These aren’t just software tools for managing customer relationships or tracking inventory in spreadsheets. They’re comprehensive ecosystems that connect every part of the business from research and development through manufacturing, regulatory compliance, sales, and customer support into one intelligent system. Think of it like upgrading from a paper map to a real-time GPS navigation system with live traffic updates. When unexpected obstacles appear, the system doesn’t just tell you there’s a problem somewhere ahead. It immediately shows you alternative routes, estimates the impact on your arrival time, and helps you make informed decisions about how to proceed based on current conditions. That’s the kind of operational intelligence medical technology companies need when tariffs hit without warning, suppliers fail to deliver, or workforce challenges emerge suddenly. Where Salesforce Transforms MedTech Operations Salesforce provides medical technology companies with a comprehensive platform that directly tackles each of these challenges while connecting every part of the business into one intelligent, responsive ecosystem. Life Sciences Cloud serves as your operational command center, providing complete visibility across your entire product lifecycle from initial concept through commercialization and beyond. When tariffs hit critical components, the platform immediately flags affected suppliers and products, calculates the financial impact across your portfolio, and enables rapid scenario planning. Product managers can instantly see which development timelines are at risk and reprioritize resources accordingly. Regulatory teams can assess compliance implications across different markets. Sourcing specialists can identify and evaluate alternative suppliers with built-in workflows that track the entire qualification process. Instead of spending weeks gathering information from disconnected systems and endless spreadsheets, companies can respond to major supply chain shocks in days or even hours. Agentforce directly solves the workforce crisis by augmenting stretched human teams with intelligent AI agents that handle substantial portions of routine work across customer service, sales, and internal operations. When a medical device company loses experienced support staff to attrition or labor disputes, Agentforce agents step in seamlessly to handle common technical inquiries, troubleshooting procedures, and product information requests. They work around the clock across multiple languages and channels, providing consistent coverage that would be impossible with human teams alone, especially during workforce shortages. This frees your remaining specialists to focus exclusively on complex cases that truly require human expertise, judgment, and relationship building. On the sales side, these AI agents qualify leads automatically, schedule product demonstrations with healthcare providers, and guide initial product selection conversations. They learn continuously from every interaction, building an ever-growing knowledge base that captures institutional expertise even as individual employees come and go. For medical technology companies struggling with sales team capacity, this means maintaining consistent, professional outreach and responsiveness to potential customers even with skeleton crews. Health Cloud creates the collaboration infrastructure that keeps dispersed, disrupted teams working together effectively despite physical separation or reduced headcount. When workforce shortages mean fewer people trying to accomplish more work, often from different locations due to remote

Digital Lending 2025 (India): Compliant Growth Under RBI’s New Directions

Compliance is the New Growth Hack And Salesforce is Your Engine. Digital Lending 2025 (India): Compliant Growth Under RBI’s New Directions August 20, 2025 10:37 pm Akash Yadav The digital lending landscape in India just got a major overhaul. With RBI issuing the Digital Lending Directions 2025 on May 8, 2025, every digital lender now faces a critical challenge: how do you scale credit operations while staying fully compliant with the most comprehensive regulatory framework India has ever seen? The answer lies not in choosing between growth and compliance, but in redesigning your entire product and platform architecture to make compliance a competitive advantage. The companies that master this integration will dominate the next decade of digital lending in India. The New Reality: Compliance as Core Architecture The 2025 Directions are not just regulatory updates—they represent a fundamental shift in how digital lending must operate. The Chief Compliance Officer (CCO) of each Regulated Entity is now accountable for certifying that all digital lending workflows comply with DLG 2025, making compliance a board-level responsibility that cannot be treated as an afterthought. This means your technology stack, product design, and business processes must be built with compliance at the core, not bolted on as an external layer. The companies that understand this shift early will have a massive advantage over those trying to retrofit compliance into existing systems. Breaking Down the New Framework: What Every Digital Lender Must Know Regulated Entities and Scope The 2025 Directions apply to all commercial banks, primary cooperative banks, state cooperative banks, central cooperative banks, all non-banking financial companies including housing finance companies, and all-India financial institutions. If you are lending digitally in India, these rules apply to you. Default Loss Guarantee: The 5% Cap Revolution The most immediate impact comes from the DLG framework. DLG cover is now capped at 5% of the disbursed portfolio and must be in the form of cash, fixed deposits, or bank guarantees. This fundamentally changes how Lending Service Providers (LSPs) can structure their partnerships with banks and NBFCs. Key implications: No revolving credit or credit card DLGs are permitted DLG must be invoked within 120 days of default unless repaid Once invoked, a guarantee cannot be reinstated For digital lending platforms, this means you need robust systems to: Track DLG utilization in real-time across your portfolio Automate DLG invocation within the 120-day window Maintain separate accounting for different portfolio segments Ensure your underwriting does not rely on DLG as a substitute for proper risk assessment LSP Governance: The New Accountability Framework LSPs can no longer collect fees directly from borrowers; REs must compensate them separately. This creates a complete restructuring of revenue flows in digital lending partnerships. Importantly, LSPs are now under RBI oversight through their contractual arrangements with REs. This means if you are an LSP, your compliance posture directly impacts your banking partners’ regulatory standing. The operational changes required: Complete separation of customer-facing fees from LSP compensation Transparent fee structures that cannot be bundled or hidden Clear contractual frameworks that define compliance responsibilities Joint liability structures between REs and LSPs for regulatory violations CIMS Registration: Your Ticket to Legitimacy All REs must report their Digital Lending Apps on RBI’s CIMS portal by June 15, 2025. The RBI will make this list publicly accessible, allowing users to verify app legitimacy. This is not just a reporting requirement—it is a fundamental shift toward transparency that will reshape customer trust and market dynamics. REs are responsible for the accuracy and timely submission of this information, which will be published by RBI without further validation. The strategic implications: Apps not registered on CIMS will lose customer trust and face regulatory action Public visibility means reputational risks are amplified Accuracy of reporting becomes critical as errors will be publicly visible Chief Compliance Officers must certify the accuracy of DLA data on CIMS portal The Cooling-Off Period: Redefining Customer Experience Borrowers now have a “cooling-off period”, determined by the RE’s board with a minimum of one day, to exit loans without penalties except a nominal processing fee. This seemingly simple requirement creates complex operational challenges. Your platform must now handle: Dynamic cooling-off periods based on different REs’ board decisions Automated loan cancellation processes Refund mechanisms for disbursed amounts Clear communication of cooling-off rights to customers Systems to prevent LSPs from charging fees during this period Key Metrics for Compliant Growth: What to Track To scale successfully under the new framework, you need to monitor compliance metrics alongside business metrics. Here are the critical KPIs: Complaint Rate Metrics Customer complaints per 1000 loans disbursed Resolution time for complaints Complaint categories trending analysis LSP vs direct RE complaint ratios Mis-selling Detection Flags Loan approval to complaint correlation Product complexity vs customer profile mismatches Excessive fee structures detection Inappropriate target customer segments NPA Performance by Channel Direct RE channels vs LSP channel NPA rates DLG invocation frequency by LSP Portfolio performance within the 5% DLG cap Time to default analysis by acquisition channel Approval TAT (Turnaround Time) Compliance End-to-end approval times including cooling-off periods System downtime impact on approval processes Compliance check delays in approval workflows Customer drop-off rates during compliance processes Product and Compliance Co-Design: The Winning Strategy The most successful digital lenders in 2025 will be those that redesign their products with compliance as a core feature, not a constraint. This means: Embedded Compliance Workflows Real-time DLG utilization tracking in loan origination systems Automated cooling-off period management Integrated KYC and customer verification processes Built-in fee transparency and disclosure mechanisms Transparent Pricing Architecture Clear separation of RE fees and LSP compensation Automated fee calculation and disclosure Dynamic pricing based on regulatory requirements Customer-friendly fee explanations and comparisons Risk Management Integration DLG-conscious underwriting models Real-time portfolio monitoring for regulatory limits Automated early warning systems for compliance breaches Integrated stress testing for different regulatory scenarios Platform Changes: Technical Architecture for Compliance Your technology platform needs fundamental changes to support compliant growth: Data Architecture Updates Separate data streams for customer fees and LSP compensation Real-time regulatory reporting capabilities

BNPL is Evolving: What Comes After Pay Later?

Next-Gen FinTech Starts Here BNPL is Evolving: What Comes After Pay Later? BNPL is Evolving: What Comes After Pay Later? August 8, 2025 12:13 pm Kartik Chopade The Buy Now, Pay Later (BNPL) revolution seemed like it happened overnight. One day we were fumbling for credit cards, the next we were splitting purchases into bite-sized installments with a few taps on our phones. But here’s the thing about revolutions – they don’t stop evolving. The BNPL landscape is shifting again, and this time it’s getting personal. Really personal. We’re moving from the one-size-fits-all “pay in 4” model to something far more sophisticated: Personalized Pay Paths. The Problem with Generic BNPL Traditional BNPL solutions treat all customers the same. Whether you’re buying a $50 pair of shoes or a $2,000 laptop, you get the same payment structure. It’s like giving everyone the same prescription glasses – sure, some people might see better, but most are still squinting. This generic approach creates friction for both businesses and customers: High-value purchases often need longer payment terms Repeat customers deserve better flexibility than first-time buyers Different income cycles (weekly, bi-weekly, monthly) require different payment schedules Shopping behavior patterns vary dramatically across customer segments Enter the New Wave: CRM + AI = Smart Payment Journeys The next generation of BNPL platforms is cracking this code by combining two powerful technologies: Customer Relationship Management (CRM) data and Artificial Intelligence. Here’s how it works: Instead of offering everyone the same “4 payments over 6 weeks” option, these smart platforms analyze individual customer data to create tailored payment journeys. They look at purchase history, payment behavior, income patterns, and even seasonal spending habits to craft payment plans that actually make sense for each person. Real-World Example Imagine Sarah, a freelance designer who gets paid monthly, and Mike, a retail worker who gets paid weekly. Traditional BNPL would offer them identical payment schedules. But with personalized pay paths: Sarah gets monthly installments aligned with her freelance payment cycle Mike gets weekly micro-payments that match his paycheck schedule Both get payment amounts optimized for their spending capacity and history The Technology Behind the Magic CRM Integration: The Data Foundation Modern BNPL platforms are integrating deeply with business CRM systems to access rich customer profiles. This includes: Purchase history and frequency Average order values and seasonal patterns Customer lifetime value calculations Communication preferences and engagement data Return and refund patterns AI-Powered Personalization Machine learning algorithms process this CRM data to: Predict optimal payment schedules based on individual cash flow patterns Calculate personalized credit limits using holistic customer profiles Identify the best communication cadence for payment reminders Suggest upsell opportunities at the right moments in the payment journey Better Engagement Through Personalization This isn’t just about making payments more convenient – it’s about creating fundamentally better customer relationships. For Customers Reduced financial stress: Payment schedules that align with actual income cycles Higher approval rates: AI considers more factors than traditional credit scoring Flexible adjustments: Plans that adapt to changing circumstances Proactive communication: Reminders and updates delivered when and how customers prefer them For Businesses Lower default rates: Payment plans matched to customer capacity reduce missed payments Increased conversion: More customers can afford purchases with personalized terms Higher customer lifetime value: Better payment experiences drive repeat purchases Improved cash flow predictability: AI helps forecast payment patterns more accurately The Competitive Advantage Companies implementing personalized pay paths are seeing impressive results: 25-40% reduction in payment defaults compared to generic BNPL 15-30% increase in average order values Higher customer satisfaction scores and Net Promoter Scores Improved operational efficiency through automated, intelligent payment management What This Means for Your Business If you’re currently using traditional BNPL solutions, it might be time to evaluate next-generation alternatives. The businesses that will thrive in the evolving payments landscape are those that treat each customer as an individual, not a demographic. Look for BNPL partners that offer: Deep CRM integration capabilities AI-driven personalization engines Flexible payment structure options Advanced analytics and reporting White-label customization options The Future is Personal We’re moving toward a world where every aspect of the shopping experience adapts to individual preferences and circumstances. Payments are no exception. The question isn’t whether personalized pay paths will become the standard – it’s how quickly your business will adopt them. Because in a world where customers have endless choices, the companies that understand them as individuals, not just credit scores, will be the ones that win their loyalty and their wallets. Latest Post 08Aug Blogs BNPL is Evolving: What Comes… Next-Gen FinTech Starts Here BNPL is Evolving: What Comes After Pay Later? BNPL is Evolving:… 07Aug Blogs The $30 Billion ‘Hidden Profit’… Next-Gen FinTech Starts Here The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How… 07Aug Blogs The Million-Dollar Mistake: Why FinTechs… Next-Gen FinTech Starts Here From Spreadsheet Chaos to Smart CRM: Why FinTechs Can’t Afford to…

The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It

Next-Gen FinTech Starts Here The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It The $30 Billion ‘Hidden Profit’ Layer in FinTech — And How CRM AI is Unlocking It August 7, 2025 2:17 pm Darpan Karanje Picture this: Your fintech company has thousands of customers using your core product, but you’re only capturing a fraction of their potential value. Meanwhile, your competitors are quietly building deeper relationships and higher lifetime values with similar customer bases. The difference? They’ve discovered the hidden profit layer that sits between customer acquisition and churn. This isn’t speculation. Recent industry analysis suggests there’s approximately $30 billion in unrealized revenue sitting dormant across fintech companies worldwide — money that’s hidden in plain sight within existing customer relationships. The key to unlocking it lies in combining behavioral data with intelligent CRM automation to drive strategic cross-selling and maximize customer lifetime value. If you’re a decision-maker in fintech, this represents one of the most significant growth opportunities available today. Here’s how smart companies are capitalizing on it. What Exactly Is This ‘Hidden Profit Layer’? The hidden profit layer refers to the untapped revenue potential within your existing customer base. Most fintech companies excel at acquiring customers for their primary product — whether that’s a payment processor, lending platform, or investment app. But they often miss the goldmine of additional services these same customers would gladly purchase. Consider a typical scenario: A small business signs up for your payment processing solution. They’re happy with the service, but you never discover they also need invoice management, expense tracking, or business loans. Meanwhile, they’re purchasing these services from your competitors, often at higher prices than you could offer. The hidden profit layer emerges when you: Identify cross-sell opportunities early in the customer journey Understand behavioral patterns that indicate readiness to buy Deliver personalized recommendations at the right moment Automate follow-up sequences that nurture interest into purchases Research shows that acquiring a new customer costs 5-25 times more than selling to an existing one. Yet most fintech companies allocate 80% of their resources to acquisition and only 20% to expansion. This imbalance represents massive missed opportunities. How Behavioral Data Reveals Customer Intent Your customers are constantly sending signals about their needs, interests, and purchasing intent. The challenge is recognizing and acting on these signals before competitors do. Behavioral data in fintech context includes: Transaction Patterns: How often customers use your service, average transaction sizes, seasonal variations, and spending categories can reveal unmet needs. A customer processing high-volume B2B payments might need cash flow management tools. Product Usage Depth: Customers who fully utilize your core features are prime candidates for complementary services. Someone maximizing your budgeting tools might be ready for investment products. Support Interactions: The questions customers ask support teams often reveal pain points that additional products could solve. Frequent inquiries about multi-currency support might indicate international expansion needs. Platform Engagement: Time spent in different app sections, feature adoption rates, and content consumption patterns provide insights into customer priorities and interests. External Indicators: Credit score changes, business growth signals, or life events (detected through permissioned data sources) can trigger relevant product recommendations. The magic happens when you analyze these data points collectively rather than in isolation. A customer showing increased transaction volume, exploring advanced features, and asking about integration options is displaying classic expansion signals. The Role of CRM AI in Unlocking Value Traditional CRM systems excel at organizing customer information, but they’re reactive by nature. You enter data, create tasks, and hope your team follows up appropriately. CRM AI transforms this dynamic by making your customer relationship management proactive and predictive. Here’s how AI-powered CRM automation drives results: Predictive Scoring: AI algorithms analyze behavioral patterns to assign expansion scores to each customer. Instead of guessing who might be interested in additional products, you get data-driven prioritization of your best opportunities. Automated Trigger Campaigns: When customers exhibit specific behaviors, AI can automatically initiate personalized outreach sequences. A customer who starts processing international payments might receive targeted information about foreign exchange services. Dynamic Content Personalization: AI customizes email content, app recommendations, and product suggestions based on individual customer profiles and behaviors. This increases relevance and conversion rates significantly. Optimal Timing Intelligence: AI identifies the best times to approach each customer with cross-sell opportunities, maximizing the likelihood of positive responses while avoiding over-communication. Conversation Intelligence: AI can analyze support tickets, sales calls, and customer communications to identify sentiment, extract needs, and recommend next best actions for account managers. The result is a CRM system that doesn’t just store customer information — it actively identifies opportunities and orchestrates the right interactions at the right time. Real-World Impact: The Numbers Don’t Lie Companies implementing AI-driven CRM strategies in fintech are seeing remarkable results: Cross-sell conversion rates increase by 40-60% when recommendations are based on behavioral triggers rather than broad market segments Customer lifetime value grows by an average of 35% within the first year of implementation Time to revenue expansion decreases from months to weeks as automated systems identify and nurture opportunities faster than manual processes Account manager productivity improves by 50% as AI handles routine identification and initial outreach, allowing humans to focus on high-value relationship building One mid-sized payment processor implemented behavioral AI and discovered that customers who used their mobile app more than 10 times per month were 4x more likely to adopt additional financial products. By automatically triggering personalized campaigns for these high-engagement users, they increased their average revenue per customer by 42% in eight months. Implementation Strategy: Where to Start Successfully unlocking your hidden profit layer requires a systematic approach: Phase 1: Data Foundation Start by auditing your current data collection and ensuring you’re capturing meaningful behavioral signals. This might require updating your tracking infrastructure or integrating new data sources. Phase 2: AI Integration Choose CRM AI tools that align with your existing tech stack and can process fintech-specific behavioral patterns. Look for solutions that offer pre-built models for financial services rather than

The Million-Dollar Mistake: Why FinTechs Still Running on Spreadsheets Will Lose in 2025

Next-Gen FinTech Starts Here From Spreadsheet Chaos to Smart CRM: Why FinTechs Can’t Afford to Ignore Salesforce in 2025 The Million-Dollar Mistake: Why FinTechs Still Running on Spreadsheets Will Lose in 2025 August 7, 2025 6:06 am Preeti Yadav Picture this: Your fintech startup just closed another funding round, your user base is exploding, and your team is scrambling to keep up with customer inquiries scattered across emails, Slack threads, and yes, that dreaded master spreadsheet that somehow became your customer database. Sound familiar? You’re not alone. As we move deeper into 2025, fintech companies are facing an uncomfortable truth: the scrappy, bootstrap methods that got them to Series A won’t cut it for sustainable growth. While traditional financial institutions lumber forward with legacy systems, agile fintechs have a golden opportunity to leapfrog the competition with smart customer relationship management. The question isn’t whether you need a proper CRM system. It’s whether you can afford to keep running your growing business on digital sticky notes and prayer. The Hidden Cost of Spreadsheet Management Let’s talk numbers for a moment. Your average fintech employee spends roughly 2.5 hours per day hunting for customer information across different platforms. Multiply that by your team size, then by your hourly rates, and you’re looking at thousands of dollars in lost productivity every single week. But the real damage goes deeper than time costs. When your customer success manager can’t quickly access a client’s transaction history during a support call, or when your sales team loses track of warm leads because they’re buried in an Excel file someone forgot to update, you’re not just losing efficiency. You’re losing trust, deals, and ultimately, competitive advantage. The financial services industry is built on trust and relationships. Every fumbled interaction, every delayed response, every “let me get back to you on that” chips away at the professional image you’ve worked so hard to build. Why Traditional CRMs Fall Short for FinTechs Here’s where many fintech leaders make their first mistake: they assume any CRM will solve their problems. They grab the first affordable solution they find, set it up over a weekend, and wonder why adoption rates are dismal six months later. Generic CRMs weren’t designed for the unique challenges of financial technology companies. They can’t handle complex compliance requirements, struggle with multi-layered approval processes, and offer little insight into the customer financial journey that’s so crucial for fintech success. Consider these fintech-specific pain points: Regulatory compliance tracking across multiple jurisdictions Integration with payment processors and banking APIs Real-time fraud monitoring and risk assessment Complex customer onboarding workflows with KYC requirements Multi-stakeholder deals involving banks, regulators, and end users Your basic CRM treats a customer as a customer. But in fintech, you need to understand whether someone is a retail user, institutional client, compliance officer, or integration partner, and tailor your entire relationship management strategy accordingly. The Salesforce Advantage: Built for Complex Growth This is where Salesforce changes the game entirely. Unlike one-size-fits-all solutions, Salesforce was designed from the ground up to handle complex business relationships and intricate sales cycles. For fintech companies, this translates into several game-changing advantages. Advanced Integration Capabilities Salesforce doesn’t just store customer data; it becomes the central nervous system of your entire operation. Through its robust API ecosystem, you can seamlessly connect your payment processors, compliance tools, risk management systems, and customer support platforms into one unified view. Imagine having real-time transaction data, compliance status, support ticket history, and sales pipeline information all accessible from a single dashboard. Your team can finally see the complete customer picture without jumping between systems. Customizable Workflows for Financial Services Every fintech has unique processes, and Salesforce’s workflow automation capabilities let you codify your business logic directly into your CRM. Whether you need multi-stage approval processes for enterprise deals or automated compliance alerts based on transaction patterns, Salesforce can handle the complexity. This isn’t just about saving time; it’s about ensuring consistency and reducing human error in processes where mistakes can have serious regulatory and financial consequences. Scalability That Grows With You Perhaps most importantly for fast-growing fintechs, Salesforce scales seamlessly from startup to enterprise. The same system that manages your first 100 customers can handle 100,000 without requiring a complete overhaul of your processes. As you expand into new markets, launch additional products, or acquire other companies, Salesforce adapts to your evolving needs rather than constraining your growth. Real-World Impact: What Success Looks Like Let’s get practical about what this transformation actually means for your day-to-day operations. Your sales team stops losing deals because they now have complete visibility into each prospect’s engagement history, technical requirements, and decision-making timeline. They can prioritize leads based on actual data rather than gut instinct. Your customer success team can proactively identify at-risk accounts by analyzing usage patterns, support ticket trends, and payment behaviors all within a single platform. Instead of reacting to churn, they’re preventing it. Your compliance team gets automated alerts about regulatory changes affecting specific customers, ensuring you stay ahead of requirements rather than scrambling to catch up during audits. Most importantly, your leadership team finally has reliable forecasting data. You can make strategic decisions based on actual pipeline metrics, customer lifetime value calculations, and market trend analysis instead of educated guesses. Making the Transition: Overcoming Implementation Hurdles The biggest barrier to CRM adoption isn’t technical; it’s human. Your team has found workarounds for existing chaos, and change feels risky when you’re moving fast and breaking things. Successful Salesforce implementations for fintechs follow a few key principles: Start with your most painful process first. Don’t try to digitize everything at once. Pick the workflow that causes the most daily frustration and nail that implementation before moving to the next challenge. Involve your team in the design process. The people who will use the system daily should have input into how it’s configured. This builds buy-in and ensures the final setup actually matches how work gets done. Plan for integration from day one. Your CRM shouldn’t

FinTech’s Silent Killer Bad Data, Worse Decisions

Next-Gen FinTech Starts Here The Hidden Enemy of Every FinTech: Bad Data in, Bad Decisions Out FinTech’s Silent Killer Bad Data, Worse Decisions August 5, 2025 5:43 am Sneha Pal Picture this: Your FinTech is humming along, processing thousands of applications daily, when suddenly your risk models start flagging legitimate customers as high-risk while approving questionable loans. Your conversion rates plummet, defaults spike, and your compliance team is pulling their hair out. What went wrong? The culprit is often hiding in plain sight: bad data. In an industry where split-second decisions can make or break profitability, the quality of your data isn’t just important—it’s everything. Yet a staggering 60% of FinTechs are still relying on manual onboarding processes or broken APIs that feed garbage into their decision engines. When your data foundation is shaky, every business-critical decision built on top of it becomes a gamble. Let’s dive into how poor data quality is silently sabotaging FinTech operations and what you can do about it. The Scale of the Problem: Why FinTechs Are Drowning in Bad Data The numbers don’t lie. While traditional banks have had decades to refine their data processes, many FinTechs are growing so fast they’re duct-taping solutions together. Manual data entry, inconsistent API integrations, and rushed implementations create a perfect storm of data quality issues. Consider what happens during a typical customer onboarding process. Information flows from multiple sources: credit bureaus, bank statements, identity verification services, and customer-provided data. Each touchpoint is an opportunity for errors to creep in—from simple typos to systemic integration failures. The result? Clean, actionable data becomes the exception rather than the rule. And in FinTech, bad data doesn’t just sit quietly in a database—it actively makes decisions that affect your bottom line. How Bad KYC Data Turns Compliance Into a Nightmare Know Your Customer (KYC) processes are your first line of defense against fraud and regulatory violations. But when KYC data is incomplete, outdated, or just plain wrong, it creates cascading problems throughout your entire operation. Bad KYC data manifests in several ways: Incomplete customer profiles that leave gaps in risk assessment Outdated information that doesn’t reflect current customer circumstances Inconsistent data formats across different verification sources False positives that flag legitimate customers as suspicious Missing red flags that should trigger additional scrutiny When your KYC foundation is compromised, you’re not just risking regulatory penalties—you’re making it harder to serve legitimate customers while potentially opening doors to bad actors. The ripple effects touch everything from customer experience to operational costs. The Risk Scoring Catastrophe: When Models Make Wrong Calls Risk scoring models are only as good as the data they consume. Feed them bad information, and they’ll confidently make terrible decisions—often at scale. Here’s where things get particularly painful. Modern FinTechs rely on sophisticated algorithms that weigh hundreds of data points to assess creditworthiness and fraud risk. These models are incredibly powerful when they have clean, consistent inputs. But introduce data quality issues, and they become expensive liability generators. Common data problems that wreck risk scoring include: Income data inconsistencies leading to incorrect affordability assessments Employment verification gaps that skew stability calculations Credit history inaccuracies that misrepresent payment behavior Identity verification errors that create false fraud signals Transaction data anomalies that trigger unnecessary alerts The cruel irony is that the more sophisticated your risk models become, the more vulnerable they are to data quality issues. A single corrupted data field can throw off an entire risk calculation, leading to approved loans that should be declined or rejected applications from your best customers. Lead Quality Degradation: When Marketing Meets Reality Your marketing team celebrates a successful campaign that generated thousands of leads. Your sales team starts working them, only to discover that half the contact information is wrong, the demographic data doesn’t match your target profile, and the lead scores are based on incomplete information. This scenario plays out daily in FinTechs where data quality issues affect lead generation and qualification processes. When customer data is inconsistent or inaccurate from the moment someone enters your funnel, it creates friction at every subsequent touchpoint. Poor lead data quality typically results in: Wasted sales resources on unqualified prospects Incorrect personalization that damages customer experience Skewed conversion metrics that mislead strategy decisions Higher customer acquisition costs due to inefficient targeting Reduced trust in data-driven marketing initiatives The hidden cost here isn’t just the immediate inefficiency—it’s the long-term erosion of confidence in your data systems across the organization. Underwriting Logic Gone Wrong: The Domino Effect Underwriting is where all your data streams converge to make the ultimate decision: approve or decline. It’s also where bad data does its most expensive damage. Modern underwriting systems process applications in real-time, evaluating everything from credit scores to bank transaction patterns. When the underlying data is flawed, these systems make decisions that look rational on the surface but are fundamentally unsound. The domino effect of bad underwriting data includes: False approvals that increase default rates and erode profitability Unnecessary declines that reduce conversion and alienate good customers Inconsistent decisions that create compliance and fairness issues Model drift as algorithms learn from corrupted training data Regulatory scrutiny when decision patterns don’t align with stated policies Perhaps most dangerous is the feedback loop effect. When bad data leads to poor underwriting decisions, and those decisions generate new data points, the system essentially trains itself to make progressively worse choices. The Business Impact: More Than Just Numbers The cumulative effect of bad data goes beyond individual transactions or customer interactions. It fundamentally undermines your ability to run a data-driven business. Consider the broader implications: Strategic decisions based on flawed analytics lead to misallocated resources Regulatory compliance becomes reactive rather than proactive Customer trust erodes when experiences don’t match expectations Operational efficiency suffers as teams spend time fixing data issues Competitive advantage diminishes when competitors have cleaner data processes In FinTech, where margins are often thin and competition is fierce, these impacts can quickly become existential threats rather than mere operational inconveniences. How Salesforce

AI Is Not the Future — It’s Already Disrupting Loan Underwriting (with Real Stats)

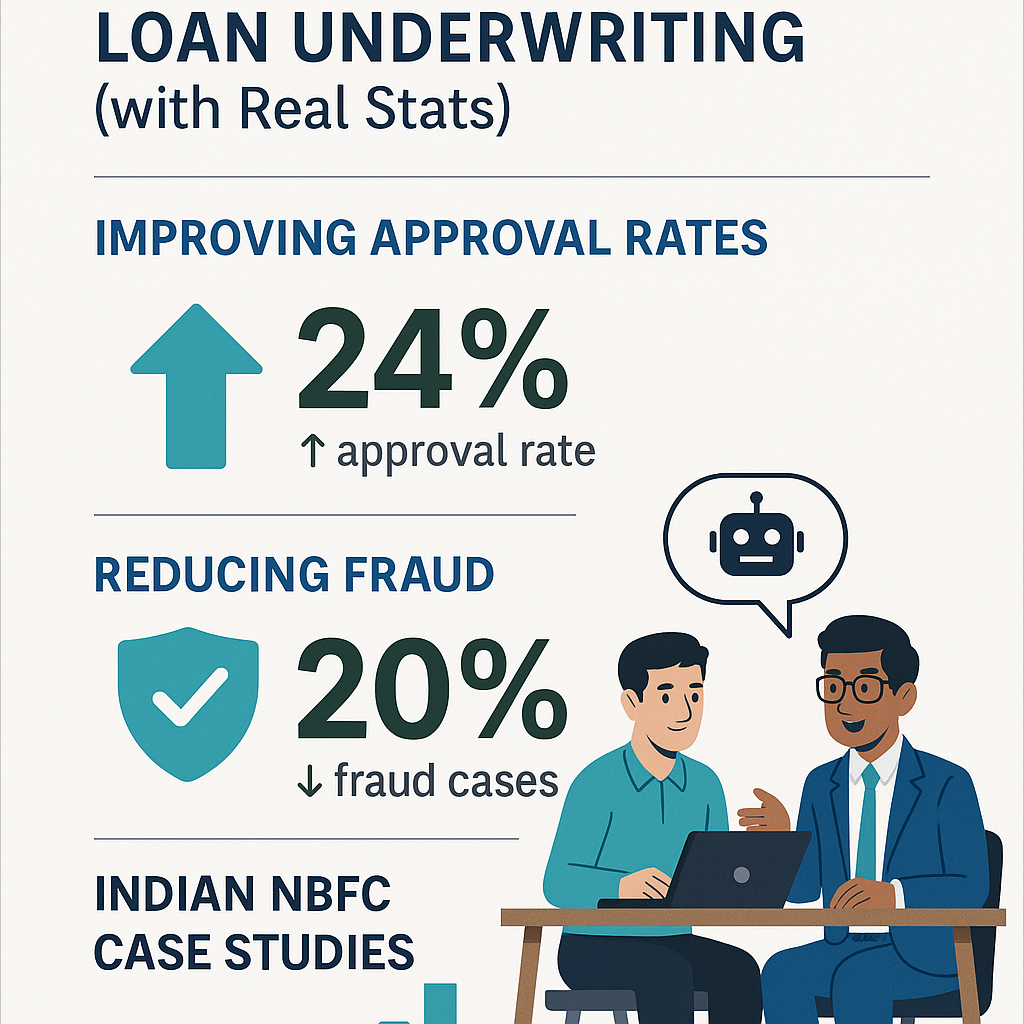

Next-Gen FinTech Starts Here The AI Lending Revolution: Faster, Smarter, Fairer AI Is Not the Future — It’s Already Disrupting Loan Underwriting (with Real Stats) August 4, 2025 2:22 pm Himanshu Sahay Picture this: A small business owner in Pune applies for a loan at 2 PM on a Tuesday. By 4 PM that same day, they receive approval, complete with personalized terms tailored to their specific risk profile. No endless paperwork. No weeks of waiting. No human bias in the decision-making process. This isn’t a glimpse into some distant future—it’s happening right now across India’s financial landscape. AI has moved from boardroom buzzword to operational reality, fundamentally transforming how lenders assess risk, approve loans, and protect themselves from fraud. The numbers tell a compelling story: 62% of executives recognize artificial intelligence/machine learning technology (AI/ML) is elevating underwriting quality and reducing fraud, and the results are already visible in the bottom line. The Traditional Underwriting Problem: Slow, Expensive, and Often Wrong For decades, loan underwriting has been a bottleneck in the lending industry. Traditional methods rely heavily on manual processes, limited data points, and human judgment—a combination that creates several pain points: Manual credit assessment can take days or weeks, leading to frustrated customers and lost business opportunities. Human underwriters, despite their expertise, can only process a fraction of the applications that AI systems handle daily. More concerning is the consistency issue—two underwriters might reach different conclusions about the same applicant. Traditional systems also struggle with thin-file applicants—people with limited credit history who might be creditworthy but don’t fit conventional scoring models. In India, where a significant portion of the population lacks extensive credit records, this limitation has historically excluded millions from accessing formal credit. How AI Is Revolutionizing Loan Underwriting Today Lightning-Fast Decision Making AI systems can analyze hundreds of data points in seconds, dramatically reducing approval times. What once took days now happens in minutes. This speed isn’t just about convenience—it’s about competitive advantage. Lenders who can provide instant decisions capture more customers and improve their market position. Enhanced Risk Assessment Through Alternative Data Modern AI systems don’t just look at traditional credit scores. They analyze smartphone usage patterns, utility payment histories, social media behavior, and transaction patterns to create a comprehensive risk profile. This approach has proven particularly effective in emerging markets like India, where traditional credit data might be limited. Significant Cost Reduction Automation eliminates much of the manual labor involved in underwriting. AI can shorten claims processing time by 30%, ensuring that policyholders receive their settlements quickly and reducing the administrative burden on insurers. While this statistic relates to insurance, similar efficiency gains are seen in loan processing. Real Statistics: The Impact Is Measurable The transformation isn’t just theoretical—the numbers prove AI’s effectiveness: Fraud Detection Improvements: AI systems excel at identifying suspicious patterns that humans might miss. By analyzing vast datasets and recognizing subtle correlations, these systems can flag potentially fraudulent applications with remarkable accuracy. Approval Rate Optimization: improved risk assessment models leading to a reduction in losses by up to 15%. This improvement comes from AI’s ability to identify creditworthy applicants who might be rejected by traditional systems, while simultaneously catching higher-risk applications that might otherwise slip through. Processing Efficiency: The shift from manual to automated processes has reduced operational costs significantly while improving consistency in decision-making. Indian NBFC Success Stories: AI in Action Case Study 1: Digital Transformation at Scale Findings indicate that AI has reached that tipping point in India, particularly in the NBFC-P2P lending space. Several Indian NBFCs have successfully implemented AI-driven underwriting systems, resulting in faster loan disbursals and improved risk management. Case Study 2: Addressing Over-Indebtedness Concerns The Indian lending landscape faces unique challenges. As of September 2024, 8% of borrowers had active loans from four or more lenders, a sharp rise from 3.6% in 2021. AI systems help NBFCs identify these over-leveraged borrowers by cross-referencing multiple data sources and providing a more complete picture of an applicant’s financial obligations. Case Study 3: Serving the Underserved Many Indian NBFCs focus on financial inclusion, extending credit to previously underserved segments. AI enables these institutions to assess risk more accurately for applicants with limited formal credit history by leveraging alternative data sources like mobile phone usage, utility payments, and digital transaction patterns. The Technology Behind the Transformation Machine Learning Models At the heart of AI underwriting are sophisticated machine learning algorithms that continuously learn and improve. These models analyze historical loan performance data to identify patterns that predict repayment likelihood. Natural Language Processing AI systems can analyze unstructured data like customer communications, social media posts, and even voice patterns during phone conversations to assess creditworthiness and detect potential fraud. Real-Time Data Integration Modern AI platforms integrate data from multiple sources in real-time, including bank statements, GST returns, utility bills, and even psychometric assessments, creating a comprehensive applicant profile. Overcoming Implementation Challenges While the benefits are clear, implementing AI in underwriting isn’t without challenges: Data Quality and Availability: AI systems are only as good as the data they process. Ensuring clean, relevant, and up-to-date data feeds is crucial for accurate decision-making. Regulatory Compliance: Financial institutions must navigate complex regulatory requirements while implementing AI systems. Ensuring transparency and explainability in AI decisions is becoming increasingly important. Change Management: Transitioning from traditional underwriting to AI-driven processes requires significant organizational change, including staff training and process redesign. Looking Ahead: The Future Is Now The transformation of loan underwriting through AI isn’t a future possibility—it’s today’s reality. Financial institutions that haven’t started their AI journey risk being left behind as competitors offer faster, more accurate, and more inclusive lending solutions. The key to success lies in choosing the right technology partners and platforms that can seamlessly integrate with existing systems while providing the flexibility to evolve with changing market needs. How Salesforce Can Accelerate Your AI Underwriting Journey For organizations looking to implement or enhance their AI underwriting capabilities, Salesforce Financial Services Cloud offers a comprehensive platform that addresses the entire lending lifecycle. Integrated Customer

Everyone Wants Real-Time Financial Health Scoring — But Nobody’s Getting It Right

Next-Gen FinTech Starts Here Cracking the Credit Scoring Code Everyone Wants Real-Time Financial Health Scoring — But Nobody’s Getting It Right August 1, 2025 11:38 am Sangavi Singh In today’s hyper-connected financial landscape, every FinTech wants to be the company that finally cracks the code on real-time borrower assessment. The promise is tantalizing: instant decisions, reduced risk, happier customers, and competitive advantage. Yet despite billions invested in AI and analytics, most financial institutions are still making lending decisions with outdated tools and fragmented data. The problem isn’t a lack of data. With UPI processing over 640 million daily transactions in India alone, behavioral insights from CRM systems, and rich transaction histories, there’s more financial data than ever before. The real challenge is that these data streams exist in silos, like having all the pieces of a puzzle scattered across different rooms. The Broken Promise of Traditional Credit Scoring Traditional credit scoring feels increasingly outdated in our digital-first world. A credit bureau score based on historical data from months or years ago tells you very little about someone’s current financial health or future ability to repay. Consider this scenario: A freelance graphic designer has an excellent payment history but took a hit during a slow quarter six months ago. Their traditional credit score reflects that rough patch, but their current UPI transactions show steady client payments, responsible spending patterns, and growing income streams. Traditional scoring systems miss this recovery entirely. This disconnect creates two major problems: For lenders: False positives and negatives lead to lost revenue and increased defaults. Good borrowers get rejected while risky ones slip through. For borrowers: Qualified individuals face unnecessary friction, while others receive credit they cannot handle, leading to financial stress. The Data Goldmine Sitting in Silos Most FinTechs are sitting on a treasure trove of insights, but these insights are trapped in disconnected systems: UPI Transaction Data Every digital payment tells a story. Transaction frequency, merchant categories, timing patterns, and spending consistency provide real-time insights into income stability and financial behavior. Yet this data rarely flows into lending decisions in real-time. CRM Behavioral Patterns Customer relationship management systems capture how borrowers interact with financial services. Response times to notifications, app usage patterns, communication preferences, and engagement levels all signal financial stress or stability before it shows up in traditional metrics. Income Verification Challenges Most lenders still rely on static documents like salary slips or bank statements. But in a gig economy where income varies monthly, these snapshots provide limited insight into actual earning capacity or future stability. The result? Lending decisions based on incomplete pictures, leading to suboptimal outcomes for everyone involved. How Next-Generation FinTechs Are Building Real-Time Intelligence Forward-thinking financial companies are moving beyond traditional approaches by creating unified data ecosystems that connect previously isolated information streams. Dynamic Transaction Pattern Analysis Instead of waiting for monthly statements, leading FinTechs analyze transaction patterns in real-time: Cash flow timing: Regular salary deposits vs. irregular freelance payments Spending categories: Essential expenses vs. discretionary purchases Transaction velocity: Frequency and consistency of financial activity Merchant analysis: Types of businesses and services being paid This approach reveals financial health trends weeks or months before they appear in traditional credit reports. Behavioral Risk Modeling Advanced systems now incorporate behavioral analytics to understand customer financial habits: Stress indicators: Changes in app usage during financial pressure Communication patterns: Response rates to payment reminders and notifications Digital engagement: Interaction with financial education content or budgeting tools Social proof signals: Consistency across digital touchpoints These behavioral signals often predict financial distress more accurately than historical payment data alone. Real-Time Income Verification Modern income verification goes beyond static documents: Live bank statement analysis: Using Account Aggregator frameworks for real-time financial data Pattern recognition: Identifying salary, freelance, and business income streams automatically Expense ratio calculations: Understanding spending patterns relative to income Seasonal adjustments: Recognizing and accounting for income variations Unified Risk Scoring Architecture The technical breakthrough comes from API-first infrastructure that creates unified data lakes ingesting information from: UPI transaction APIs for real-time payment data Account Aggregator feeds for comprehensive financial pictures CRM interaction logs for behavioral insights External data sources for additional context validation This architecture enables real-time risk scoring that updates continuously rather than monthly or quarterly. The Competitive Advantage of Getting It Right Companies successfully implementing real-time financial health scoring are seeing significant benefits: Reduced Default Rates: Real-time verification systems can reduce fraud risks by 60-80% by cross-referencing multiple data points instantly. Faster Decision Making: Automated systems provide lending decisions in minutes rather than days, improving customer experience and operational efficiency. Better Risk Assessment: Dynamic scoring models identify both opportunities and risks that traditional systems miss, leading to more profitable lending portfolios. Customer Satisfaction: Borrowers appreciate quick decisions and feel understood when their current financial situation is accurately reflected in lending decisions. Implementation Challenges and Solutions Building real-time financial health scoring isn’t without obstacles: Data Privacy and Compliance: Handling real-time financial data requires robust security measures and regulatory compliance. Solution: Implement privacy-by-design architectures with strong encryption and audit trails. Integration Complexity: Connecting multiple data sources with different formats and update frequencies is technically challenging. Solution: Use standardized APIs and middleware platforms designed for financial data integration. Model Accuracy: Real-time models must balance speed with accuracy to avoid poor lending decisions. Solution: Implement continuous learning systems that improve with each transaction and outcome. How Salesforce Can Transform Financial Health Scoring Salesforce’s ecosystem presents unique opportunities to address the real-time financial health scoring challenge through its comprehensive platform approach. Customer 360 for Financial Services Salesforce’s Customer 360 platform can serve as the unified data layer that FinTechs desperately need. By integrating UPI transaction data, CRM behavioral patterns, and income verification into a single customer view, financial institutions can finally break down the data silos that limit current scoring approaches. The platform’s real-time processing capabilities enable instant updates to customer profiles as new financial data flows in, creating the dynamic scoring models that next-generation FinTechs require. AI and Analytics Integration Einstein AI can analyze the complex