Next-Gen FinTech Starts Here Future. Faster. UPI 3.0 July 30, 2025 7:14 am Akash Yadav Why Every FinTech Startup in India Is Betting Big on UPI 3.0 — And What You’re Missing Picture this scenario: A small business owner in Bengaluru applies for a loan at 10 AM, gets instant approval by 10:05 AM, and starts spending the credit line through UPI by 10:10 AM. No paperwork, no branch visits, no waiting for weeks. This is not a futuristic dream—this is happening right now, and it is reshaping how India thinks about credit, lending, and financial services. India is now home to 28 fintech unicorns, ranking third globally behind the US and China, and almost every single one of them is doubling down on UPI 3.0 capabilities. But what exactly is driving this massive shift, and why are startups betting their entire business models on this evolution? The UPI Revolution That Started It All UPI transformed payments in India by making digital transactions as simple as sending a text message. From processing a handful of transactions in 2016 to handling billions of transactions monthly, UPI became the backbone of India’s digital economy. But payments were just the beginning. NPCI started introducing new features under UPI 3.0 from 2024, including “Conversational Voice Payments” unveiled at the Global Fintech Fest 2024, marking a significant advancement in transaction convenience. However, the real game-changer lies not in how we pay, but in how UPI 3.0 is revolutionizing lending, credit scoring, and customer onboarding. The Credit Line Revolution: Instant Money at Your Fingertips The most significant development in UPI 3.0 is the Credit Line on UPI feature. This product empowers individuals and small businesses to obtain pre-sanctioned credit lines from banks, which can be utilized immediately for transactions through UPI. Think of it as having a pre-approved credit card that works seamlessly with UPI payments. Here is how the process works in practice: Users open a UPI app, go to the Credit or Loan section, select the ‘Credit Line option’, enter required personal and financial information, and complete KYC verification. What previously took weeks now happens in minutes. This capability is transforming how FinTech startups approach lending. Instead of building separate loan applications and payment systems, they can now offer instant credit that integrates directly with India’s most popular payment method. The result is a seamless user experience that removes friction from both borrowing and spending. Micro-Lending Gets a Major Upgrade UPI 3.0 is particularly revolutionary for micro-lending startups. Traditional micro-lending involved extensive paperwork, physical verification, and lengthy approval processes. The new UPI infrastructure changes this completely. India has launched a digital credit assessment system for MSMEs with UPI-based lending, replacing traditional collateral with transaction-based assessments. This means that small businesses can now access credit based on their UPI transaction history rather than traditional collateral or credit scores. For FinTech startups, this opens up massive opportunities. They can now offer: Instant micro-loans based on UPI transaction patterns Credit lines that activate automatically when users need them Small business loans that get approved based on payment volumes Consumer credit that adapts to spending behavior The addressable market is enormous. Small businesses and individual entrepreneurs who were previously excluded from formal credit systems can now access funding instantly through platforms they already use daily. Instant Credit Scoring: The Data Goldmine Perhaps the most exciting aspect of UPI 3.0 for FinTech startups is the treasure trove of transaction data it provides for credit scoring. Traditional credit scoring in India relied heavily on formal banking relationships and credit card usage, excluding millions of people with limited banking history. UPI transaction data tells a completely different story. It reveals: Regular income patterns through salary credits and recurring payments Spending behavior across different categories Business cash flows for merchants and service providers Financial discipline through savings and investment patterns Social connections through peer-to-peer transactions FinTech startups are building sophisticated algorithms that can assess creditworthiness within minutes using this UPI transaction data. A street vendor who receives consistent UPI payments can now qualify for business loans. A young professional with regular UPI-based salary credits can access instant personal loans without a lengthy credit history. The competitive advantage is clear: startups that master UPI-based credit scoring can approve loans faster, assess risk more accurately, and serve previously underbanked populations. KYC Automation: The Silent Game Changer Customer onboarding has always been a pain point for FinTech startups. Traditional KYC processes involved document submissions, manual verification, and regulatory compliance checks that could take days or weeks. UPI 3.0 changes this equation dramatically. As per April 2021 RBI directive, after March 31, 2022, all KYC compliant digital wallets became interoperable using the UPI system. This interoperability means that KYC verification done for one UPI-enabled service can be leveraged across multiple platforms. For FinTech startups, this translates to: Instant customer verification using existing UPI KYC data Reduced onboarding friction and higher conversion rates Lower compliance costs and faster regulatory approvals Seamless integration with banking partners who are already UPI-enabled The automation possibilities are endless. A customer who is already KYC-verified on one UPI app can instantly access services from multiple FinTech partners without repeating the verification process. The Platform Play: Why Infrastructure Matters M2P Fintech serves as a solution for enabling credit line functionality on UPI with their unified credit stack, empowering financial institutions with flexible lending solutions across various channels. This highlights how FinTech startups are not just building consumer-facing applications but also creating the infrastructure that enables UPI 3.0 capabilities. The smartest FinTech startups are positioning themselves as enablers rather than just service providers. They are building: API platforms that help traditional banks offer UPI-based credit White-label solutions for smaller financial institutions Credit scoring engines that can be licensed to multiple lenders KYC automation tools that serve the entire ecosystem This platform approach creates multiple revenue streams and reduces dependency on any single business model. Market Dynamics: The Numbers Tell the Story The India Fintech Market is expected to reach USD 44.12 billion in 2025 and

From Manual to Magical: How FinTech Companies Use Salesforce AI to Transform Collections

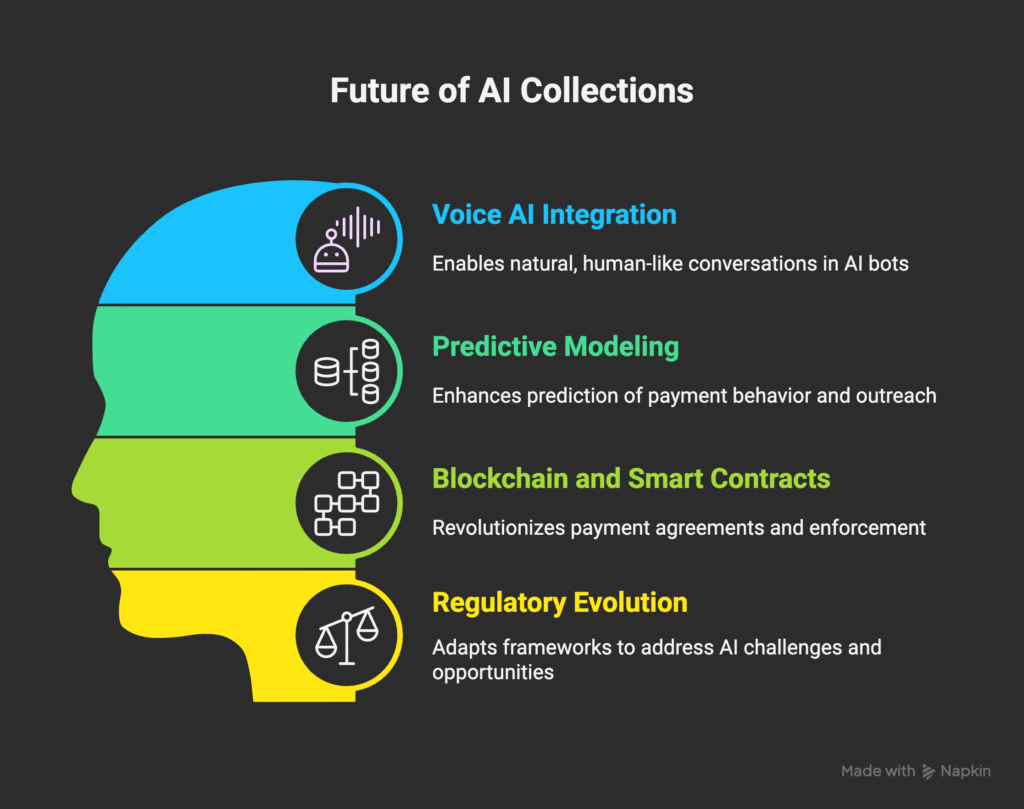

From Manual to Magical: How FinTech Companies Use Salesforce AI to Transform Collections The collections industry is experiencing a seismic shift. While most organizations still rely on human agents making countless phone calls, forward-thinking companies are deploying AI-powered bots that integrate seamlessly with WhatsApp and Salesforce CRM triggers, achieving remarkable cost reductions of up to 40%. The question isn’t whether this transformation will happen—it’s whether your organization will lead or follow. The Current State: Why Manual Collections Are Failing The Human Agent Bottleneck Traditional collections operations are plagued by inefficiencies that seem almost archaic in today’s digital age. Human agents spend hours each day making outbound calls, often reaching voicemails, disconnected numbers, or unresponsive debtors. The average collections agent can only handle 50-80 accounts per day, with success rates hovering around 15-20% for first-contact resolutions. This manual approach creates several critical problems: Scalability Limitations: As portfolios grow, organizations must hire more agents, increasing overhead costs and training complexity. Each new hire requires weeks of training and months to reach full productivity. Inconsistent Messaging: Human agents, despite training, deliver inconsistent messages and may not always follow compliance protocols perfectly. This variability can lead to regulatory issues and damaged customer relationships. Limited Operating Hours: Traditional call centers operate during business hours, missing opportunities to connect with debtors who may only be available during evenings or weekends. High Operational Costs: Between salaries, benefits, training, technology, and facility costs, the total cost per agent can exceed $60,000 annually, not including the productivity losses from sick days, vacation time, and turnover. The Communication Gap Perhaps most critically, traditional collections methods fail to meet modern consumer communication preferences. Studies show that 75% of consumers prefer text-based communication over phone calls, yet most collections operations remain phone-centric. This disconnect creates friction that reduces payment rates and increases customer frustration. The AI Revolution: Transforming Collections Through Intelligent Automation Understanding AI Collections Bots AI collections bots represent a fundamental shift from reactive to proactive collections management. These sophisticated systems leverage natural language processing, machine learning, and integration capabilities to automate the entire collections workflow while maintaining personalization and compliance. Modern AI bots can analyze debtor profiles, payment histories, and behavioral patterns to craft personalized outreach strategies. They understand context, respond to objections, negotiate payment arrangements, and seamlessly escalate complex cases to human agents when necessary. The Power of Multi-Channel Integration The most successful AI collections implementations combine multiple communication channels with robust CRM integration: WhatsApp Business Integration: With over 2 billion users worldwide, WhatsApp has become the preferred communication channel for many consumers. AI bots can initiate conversations, send payment reminders, share payment links, and even process payments directly within the chat interface. Salesforce CRM Triggers: Integration with Salesforce enables sophisticated workflow automation. When specific conditions are met—such as a payment becoming 30 days overdue—the system automatically triggers personalized bot outreach sequences tailored to the debtor’s profile and history. SMS and Email Backup: For comprehensive coverage, AI bots can seamlessly switch between channels based on response rates and customer preferences, ensuring maximum engagement. Real-World Impact: The 40% Cost Reduction Reality Breaking Down the Cost Savings Organizations implementing AI collections bots report average cost reductions of 40%, but understanding where these savings come from reveals the true power of automation: Reduced Labor Costs (60% of savings): AI bots can handle the workload of multiple human agents simultaneously. A single bot can manage thousands of accounts, working 24/7 without breaks, sick days, or vacation time. Increased Collection Rates (25% of savings): By reaching debtors through their preferred communication channels at optimal times, AI bots often achieve higher contact and payment rates than traditional methods. Operational Efficiency (15% of savings): Automated workflows eliminate manual data entry, reduce processing time, and minimize errors, creating significant operational efficiencies. Case Study: Regional Credit Union Success A regional credit union with 50,000 members implemented an AI collections bot integrated with WhatsApp and Salesforce. Within six months, they achieved: 45% reduction in collections operational costs 35% increase in first-contact payment rates 60% reduction in accounts requiring human agent intervention 90% customer satisfaction rate with the bot interaction experience The bot handled over 10,000 collection cases monthly, with human agents focusing only on complex negotiations and legal proceedings. Building Your AI Collections Bot: A Strategic Framework Phase 1: Foundation and Planning Compliance First Approach: Before any technical development, ensure your AI bot framework complies with all relevant regulations including the Fair Debt Collection Practices Act (FDCPA), Telephone Consumer Protection Act (TCPA), and state-specific collection laws. Build compliance into the bot’s core logic, not as an afterthought. Data Integration Strategy: Successful AI collections bots require comprehensive data integration. Connect your existing systems including core banking platforms, loan management systems, payment processors, and customer databases to create a unified view of each debtor’s situation. Communication Channel Setup: Establish your multi-channel communication infrastructure. Set up WhatsApp Business API access, configure SMS gateways, and ensure email deliverability. Each channel requires specific setup and compliance considerations. Phase 2: Salesforce CRM Integration Trigger Configuration: Design sophisticated trigger rules within Salesforce that initiate bot sequences based on specific criteria such as: Days past due thresholds Payment amount and frequency patterns Previous contact history and responses Customer risk scores and segmentation Seasonal or economic factors Workflow Automation: Create automated workflows that update customer records, log interactions, schedule follow-ups, and escalate cases based on bot interactions. This integration ensures seamless handoffs between automated and human processes. Real-Time Sync: Implement real-time data synchronization between your bot platform and Salesforce to ensure agents have immediate access to all bot interactions when they need to intervene. Phase 3: AI Bot Development Natural Language Processing: Develop or integrate NLP capabilities that can understand customer responses, detect payment intent, identify hardship situations, and respond appropriately. The bot should handle common scenarios like payment confirmations, dispute notifications, and arrangement requests. Personalization Engine: Build dynamic message generation capabilities that personalize communications based on customer data, payment history, and previous interactions. Personalized messages consistently outperform generic templates. Payment Integration: Integrate secure payment processing directly

Salesforce Marketing Account Engagement

Unlocking B2B Marketing Success with Salesforce Marketing Account Engagement In today’s competitive B2B landscape, marketing teams need sophisticated tools to nurture leads, align with sales, and drive revenue growth. Salesforce Marketing Account Engagement (formerly known as Pardot) has emerged as a game-changing solution that transforms how businesses approach account-based marketing and lead nurturing. What is Salesforce Marketing Account Engagement? Salesforce Marketing Account Engagement is a comprehensive B2B marketing automation platform designed to help businesses generate more qualified leads, accelerate sales cycles, and maximize marketing ROI. As part of the Salesforce ecosystem, it seamlessly integrates with Sales Cloud, providing a unified view of prospects and customers throughout their entire journey. The platform empowers marketing teams to create personalized experiences at scale, automate repetitive tasks, and deliver the right message to the right prospect at the right time. Whether you’re targeting individual leads or entire buying committees, Marketing Account Engagement provides the tools needed to orchestrate sophisticated marketing campaigns. Key Features That Drive Results Lead Scoring and Grading- One of the platform’s most powerful features is its dual approach to lead qualification. Lead scoring measures engagement levels based on actions like email opens, website visits, and content downloads. Lead grading evaluates how well a prospect fits your ideal customer profile based on demographic and firmographic data. This combination helps sales teams prioritize their efforts on the most promising opportunities. Dynamic Content and Personalization- Marketing Account Engagement enables marketers to create highly personalized experiences without creating dozens of separate campaigns. Dynamic content adjusts based on prospect attributes, behavior, and engagement history, ensuring every interaction feels relevant and valuable. Advanced Email Marketing- The platform offers sophisticated email marketing capabilities, including A/B testing, responsive templates, and automated drip campaigns. Marketers can create complex email workflows that adapt based on prospect behavior, ensuring optimal engagement throughout the customer journey. Account-Based Marketing (ABM)- With built-in ABM capabilities, Marketing Account Engagement helps teams identify and target high-value accounts. The platform provides account-level insights, enables coordinated campaigns across multiple contacts within target accounts, and offers specialized reporting to measure ABM success. The Power of Salesforce Integratio What sets Marketing Account Engagement apart is its native integration with Salesforce CRM. This connection creates a seamless flow of information between marketing and sales teams, enabling: Unified Lead Management: Prospects automatically sync between systems, ensuring both teams work with the same, up-to-date information. Closed-Loop Reporting: Marketers can track the complete customer journey from first touch to closed deal, providing clear visibility into marketing’s impact on revenue. Sales Enablement: Sales teams receive rich prospect insights, including engagement history, content consumption, and behavioral triggers, enabling more informed conversations. Real-World Applications Lead Nurturing Campaigns- A typical nurturing campaign might begin when a prospect downloads a white paper. Marketing Account Engagement can automatically enroll them in a series of educational emails, track their engagement, and trigger alerts when they show buying signals. If the prospect visits your pricing page multiple times, the system can automatically notify sales for timely follow-up. Event Marketing- For companies that rely on events and webinars, Marketing Account Engagement streamlines the entire process. From registration landing pages to automated follow-up sequences, the platform ensures no lead falls through the cracks. Post-event nurturing campaigns can be triggered based on attendance, engagement level, or specific sessions attended. Content Marketing Optimization- The platform tracks how prospects interact with your content, revealing which pieces drive the most engagement and conversions. This data helps marketers refine their content strategy and create more effective campaigns. Measuring Success Marketing Account Engagement provides comprehensive analytics that go beyond basic email metrics. Key performance indicators include: Pipeline velocity: How quickly leads move through the sales funnel Marketing qualified leads (MQLs): Prospects who meet defined criteria for sales readiness Return on investment: Direct correlation between marketing activities and revenue Account engagement: Comprehensive view of how entire buying committees interact with your brand Best Practices for Implementation Successful Marketing Account Engagement implementation requires careful planning and ongoing optimization. Start by defining clear lead scoring criteria based on your ideal customer profile and typical buying journey. Establish service level agreements between marketing and sales teams to ensure smooth lead handoffs. Content mapping is crucial for effective nurturing campaigns. Align your content with different stages of the buyer’s journey and create automated workflows that deliver the right content at the right time. Regular testing and optimization ensure your campaigns continue to improve performance over time. The Future of B2B Marketing As B2B buying processes become more complex and involve larger committees, platforms like Marketing Account Engagement become increasingly valuable. The ability to orchestrate personalized experiences across multiple touchpoints while maintaining visibility into the entire customer journey is essential for modern marketing success. Organizations that leverage Marketing Account Engagement effectively often see significant improvements in lead quality, sales conversion rates, and overall marketing efficiency. The platform’s AI-powered insights and automation capabilities free up marketers to focus on strategy and creativity rather than manual tasks.

DevOps trends

DevOps Trends DevOps trends January 16, 2025 admin 12:46 pm The world of DevOps is constantly evolving, driven by new technologies, automation, and the need for faster and more secure software delivery. As we move through 2025, organizations are increasingly adopting modern DevOps practices to enhance efficiency, scalability, and security. Here are the top DevOps trends that are reshaping the industry this year: AI and Machine Learning in DevOps AI-powered automation is revolutionizing DevOps by optimizing workflows, reducing human errors, and predicting system failures before they happen. Machine learning models are now being used to analyze logs, detect anomalies, and improve CI/CD pipeline performance. Key Impact: Automated root cause analysis for faster troubleshooting AI-driven code review and test automation Predictive analytics for system failures Latest Post 07Mar Case Study Optimizing Field Operations for AquaFlow… 07Mar Case Study Scaling Operations for InnoTech Startups 07Mar Case Study Streamlining Patient Management for Care…

Salesforce best practices

Welcome to WordPress. This is your first post. Edit or delete it, then start writing!

Zoho tips

Welcome to WordPress. This is your first post. Edit or delete it, then start writing!